India’s fertiliser stocks look comfortable on paper.

As of March 10, inventories stood at 180.12 lakh metric tonnes, up 36.6% from a year earlier. That is the kind of number that makes a shock feel manageable, almost routine. But it may be the wrong number to stare at.

Stocks are not supply. Stocks are time bought in advance. The real question is whether the next replenishment wave keeps arriving. India is already talking to Russia, Belarus, Morocco and Indonesia to boost fertiliser imports while keeping fertiliser plants supplied with at least 70% of average gas consumption. That is not a picture of panic. It is a picture of a system trying to stay ahead of the clock.

Everyone is watching gas. That makes sense. Gas is visible. Gas makes headlines. Gas is what gets rationed first, what households notice first, what governments scramble to protect first. But the real stress in this shock sits one layer below, in something far less visible and far harder to substitute: sulphur.

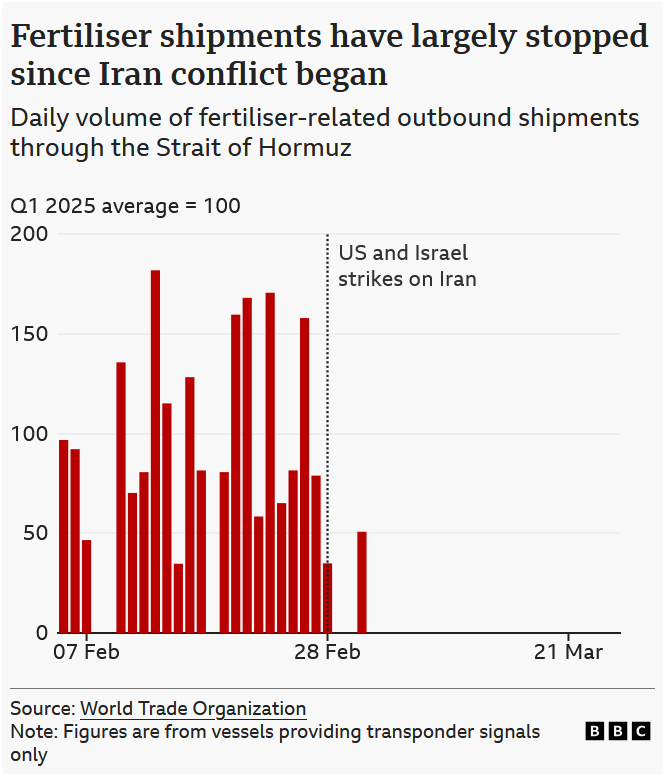

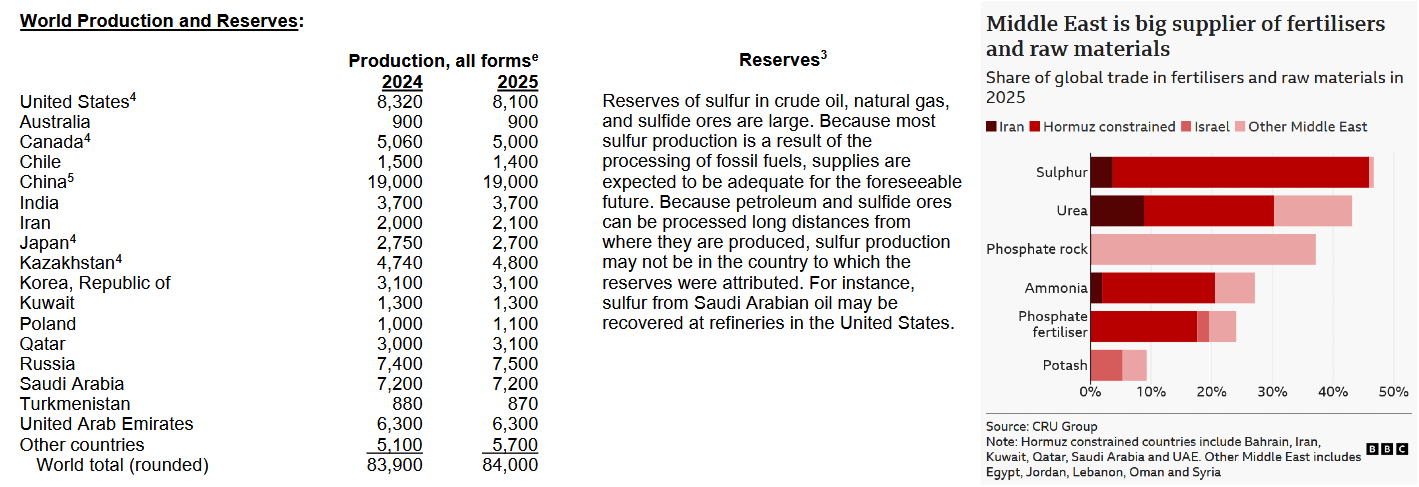

The Strait of Hormuz is not just an oil chokepoint. It is a chokepoint for sulphur, sulphuric acid, fertiliser feedstocks and, downstream, food itself. The Middle East accounts for about a quarter of global sulphur production, and about half of seaborne sulphur trade passes through Hormuz. When the corridor tightens, sulphur does not just become more expensive. It becomes uncertain. And uncertainty is what breaks industrial systems.

That is the break in the lazy story. The obvious framing says this is an oil shock, maybe a gas shock, maybe a bit of inflation, maybe a little stress in shipping. But sulphur is the hidden input that connects all of them. It is usually recovered as a by-product of refining sour crude and processing gas. So when shipping routes are disrupted, or when energy processing slows, sulphur supply can tighten even if no one has formally declared a sulphur shortage. The dependency is inverted: the thing that looks secondary turns out to be the constraint everyone else depends on.

Why does sulphur matter so much?

Because sulphur becomes sulphuric acid, and sulphuric acid is one of industry’s basic working chemicals. It is central to fertiliser manufacturing, and it is also crucial in acid-intensive metal processing. More than 60% of sulphuric acid goes into fertilisers. In simple terms: no sulphur, less acid; less acid, less fertiliser. That matters because fertiliser is not a side story in India. It is one of the hardest-to-fake inputs in the whole economy.

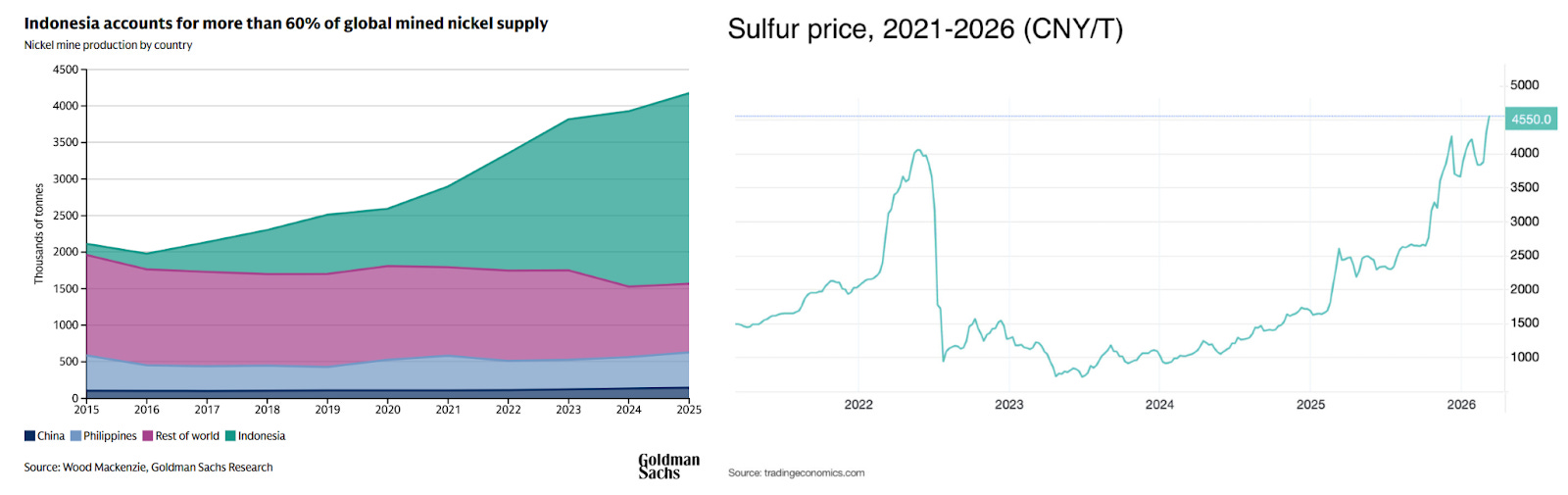

The metal angle matters too, but only as evidence that the same bottleneck is already spreading. Indonesia, which produces more than half of global nickel, imports roughly 75% of its sulphur from the Middle East.

Some HPAL plants hold only one to two months of sulphur inventory. That is not much slack for a system that depends on imports moving through a contested maritime corridor. Sulphur prices were already around $500 a tonne before the latest conflict and then rose another 10% to 15%. Sulphuric acid had already been in a brutal multi-year tightness before the latest disruption. Price is doing the work before the shortage is fully visible.

That is why this story is not really about oil. It is about the timing system underneath industry. Sulphuric acid is bulky, corrosive and expensive to move over long distances, so this is not a market that can pivot instantly. New acid capacity cannot be switched on quickly. Alternative sulphur flows take time to redirect. That means the first effect is not “outage.” It is “friction.” Then “price.” Then “allocation.” Then, if the disruption lasts, “curtailment.”

The technical part is straightforward. In mining, sulphuric acid is used mainly in leaching. Ore is treated with acid so metals can be dissolved, separated and recovered. That makes it central to hydrometallurgy, especially HPAL nickel, oxide copper leaching, and some uranium, rare earth and titanium sulphate-route processing chains. Without acid, a large share of low-grade or chemically difficult ore cannot be processed economically at scale. That is why a sulphur shock is not just a commodities story. It is a production-physics story.

Copper and cobalt are exposed next. Africa’s copper belt imports about two million tons of sulphur a year, with most of it coming from the Middle East, for oxide copper leaching. The Democratic Republic of Congo supplies roughly 70% of global mined cobalt, which also relies on acid-leach chains. Some operations are insulated because they have captive acid plants or by-product acid from smelters. Others are not. That distinction matters. In tight conditions, sulphuric acid stops being a side-product and starts behaving like a critical mineral in its own right.

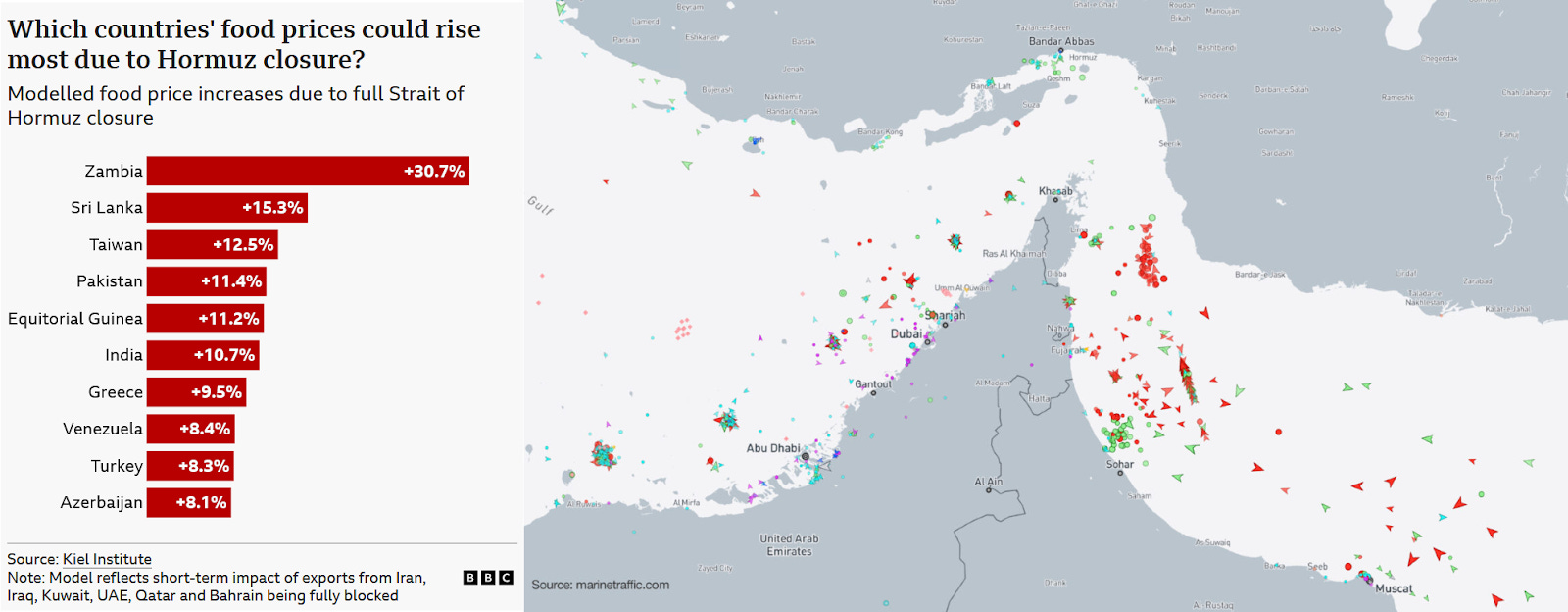

India sits at the sharp end of the fertiliser version of that same logic. Nearly two-thirds of its sulphur imports come from West Asia. The country has been trying to diversify fertiliser supply because the Middle East tensions are colliding with planting season and with other trade disruptions. India imported about $3.7 billion worth of fertilisers from West Asia, and the biggest risk is not just the current stockpile. It is the refill channel behind it.

So the real transmission looks like this:

Hormuz disruption → sulphur disruption → sulphuric acid tightness → fertiliser cost pressure → planting-season risk → food inflation.

That chain matters because the shock is delayed. Farmers do not need a clean shortage to change behaviour. They react to price, timing and confidence. If fertiliser availability becomes uncertain, application rates can fall, purchases can be delayed, and crop choices can shift before any official crisis appears. A separate analysis of the same crisis argued that the Strait of Hormuz disruption is not just an oil-market story, but a food-security story too. That is exactly right. The market is not just short of commodities. It is short of slack.

That is the deeper lesson. Modern economies are built not only on big visible commodities like oil and gas. They are built on by-products, intermediates and schedules. The stuff nobody tracks until it stops moving. Sulphur is one of those hidden hinges. It is not glamorous. It is not usually strategic. But in a crisis, it becomes strategic very quickly because it sits underneath things that absolutely are strategic: food, metals, and industrial continuity.

The question now is not how high oil goes. It is whether enough sulphur keeps moving to keep fertiliser plants fed through the next crop cycle. Because if the answer is no, the story will not stay in the chemical market. It will move into farms, food prices, subsidies and politics.

Soon, it won’t be about gas.

It’ll be about sulphur.

Disclaimer: I am not a registered SEBI Research Analyst and anything in the above article should not be construed as a recommendation. This should be read solely for education purposes.