The RBI’s move last week looked like a currency story. It was actually a market-structure story.

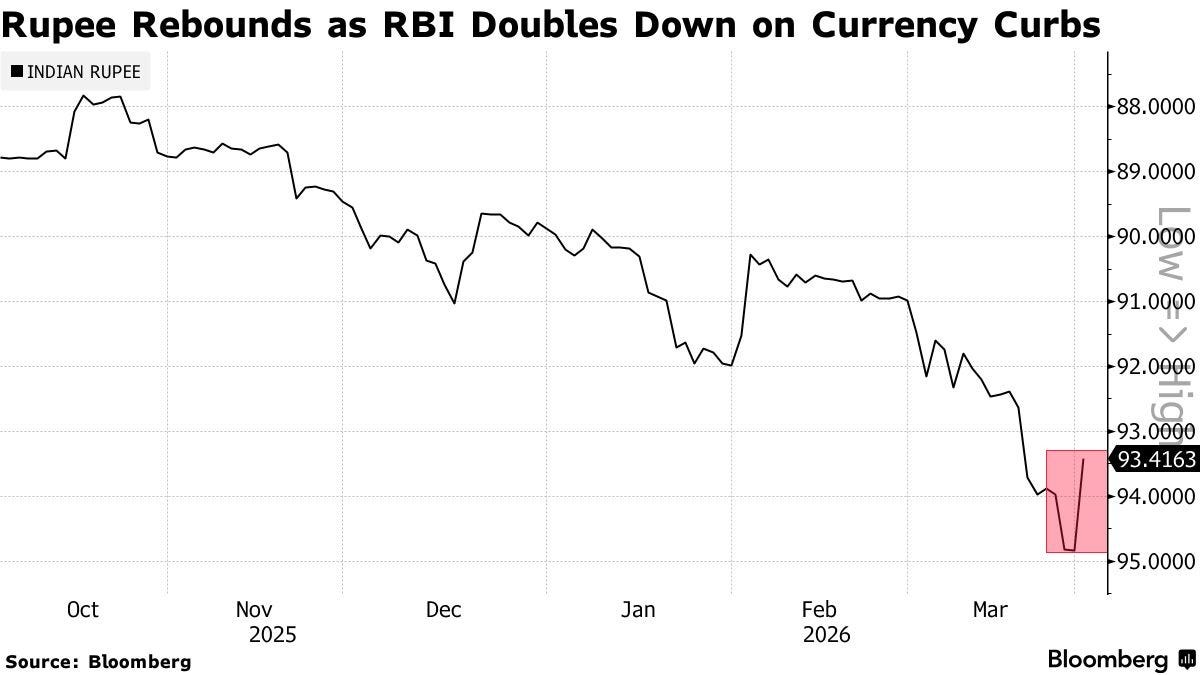

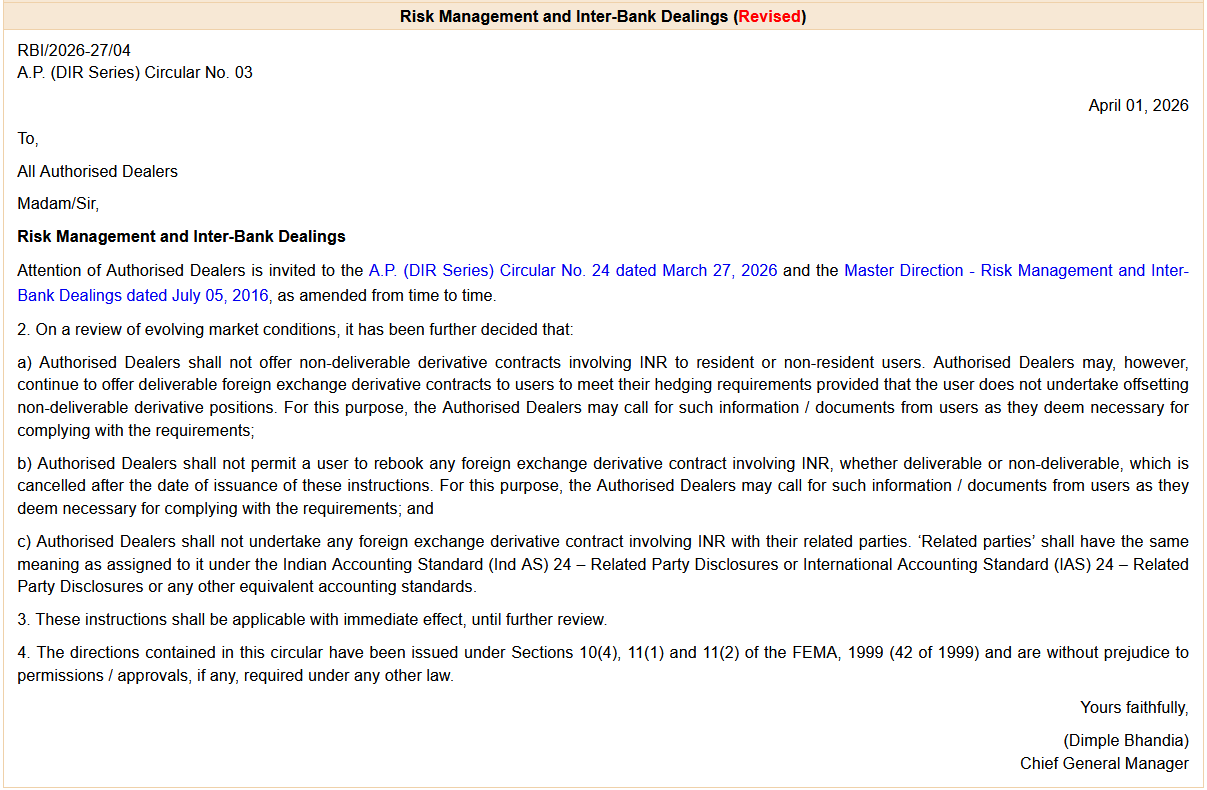

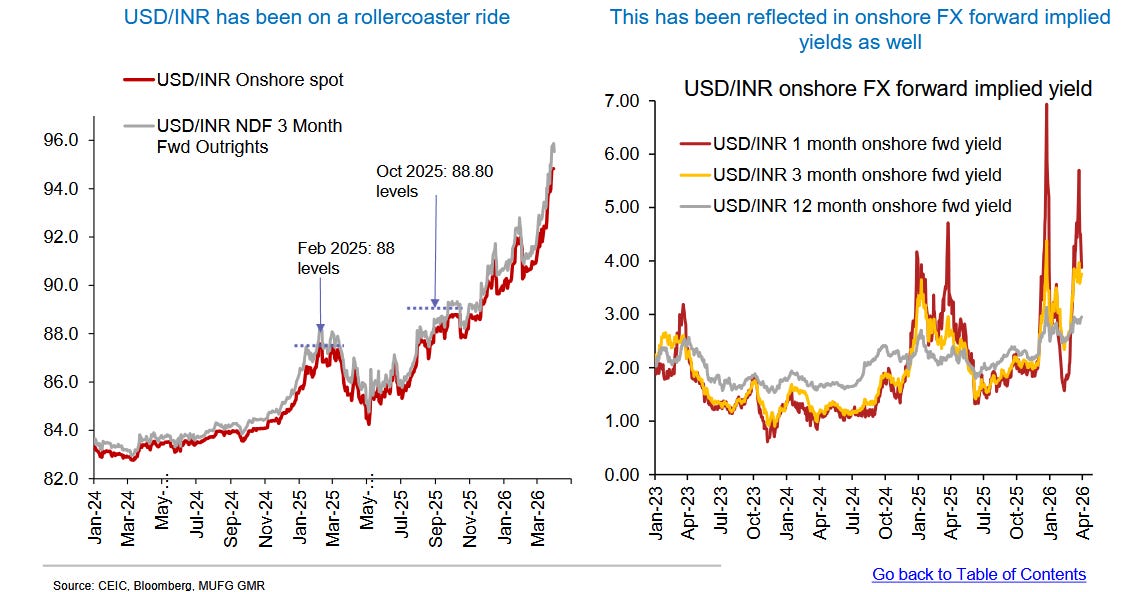

First came tighter limits on banks’ net open rupee positions. Then came the bigger blow: a ban on rupee non-deliverable forwards, or NDFs. That hit an offshore market of roughly $149 billion a day, about twice the size of India’s onshore FX market. The rupee snapped back sharply, rising 166 paise on April 2, the best since over a decade. But the more important point is not that the rupee bounced. It is that the RBI chose to change the plumbing of the market to stop the pressure.

The obvious story is too neat

The easy read is comforting: the central bank saw speculators leaning on the rupee, stepped in, and restored order. Strong RBI, weaker traders, stable currency. Clean ending.

But that is not what happened.

What the RBI did was more serious. It narrowed the part of the currency market where global capital could lean against the rupee, because the pressure had become harder to manage inside the old setup. The NDF market did not appear out of nowhere. It grew while the RBI was trying to deepen offshore-onshore integration as part of rupee internationalisation. Then the system hit a wall. Banks hit position caps. Some risk moved to corporates. The rupee still broke lower. So the RBI closed the escape hatch.

That is not a simple defence. It is a trade-off.

The number that looks calm is not calm

Now look at inflation.

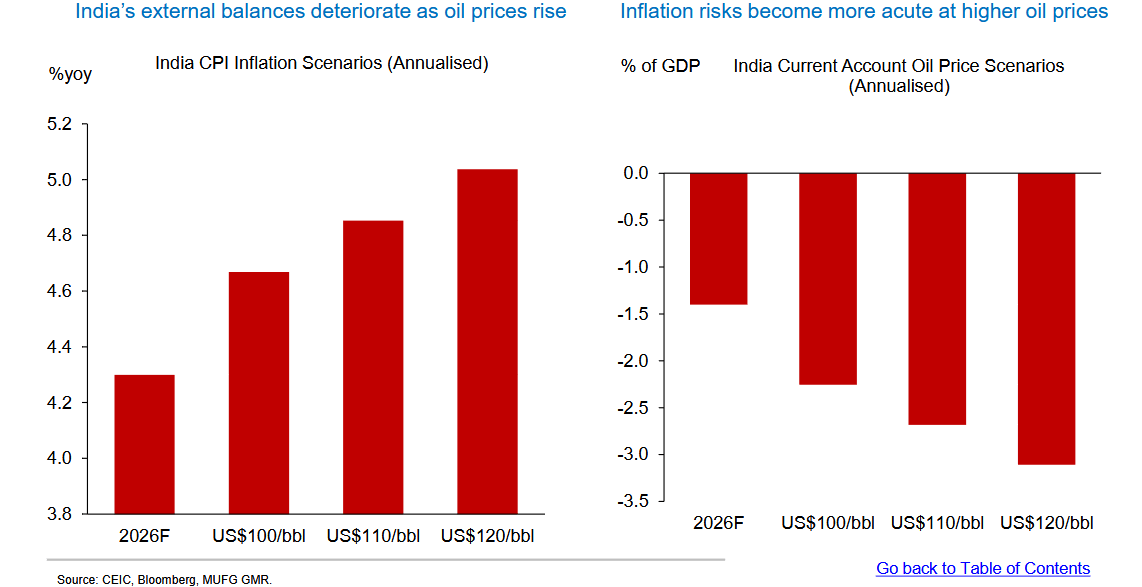

Headline CPI at 3.21% looks almost benign. That is the problem. It makes the current shock look smaller than it is. The number is not fake. It is just late.

Imported inflation has not fully shown up yet. Fuel pass-through is incomplete. Food weights have changed in the new CPI series. Some of the pressure is still sitting inside the balance sheets of oil marketing companies, not inside the official inflation print. In other words, the pain has not disappeared. It has been delayed, redistributed, and partly hidden.

That matters because investors often mistake a clean CPI print for a clean macro backdrop. It is not clean. It is lagged.

If crude stays high and the rupee stays weak, the gap between market reality and reported inflation will close. By then, the damage will already be moving through consumer prices, import costs, company margins, and political choices on fuel pass-through. The number is not lying. It is arriving after the fact.

The MPC is now in a trap

This is why the April MPC is more than a routine meeting.

On paper, the RBI has room. Repo is at 5.25%, after 125 basis points of cuts over the past year. CPI is still below target. Growth is not collapsing. That sounds manageable.

It is not.

The central bank is now facing a classic stagflation setup: weaker growth from external shocks, and higher inflation pressure from the same shock. The rupee is under pressure. Crude is expensive. Foreign capital is leaving. Bond markets are repricing duration risk. Every move now has a cost. A hike helps the rupee but hurts growth. A hold protects growth optics but risks more currency pressure. A pause looks neutral, but in this environment it is not neutral at all.

That is the real dilemma.

The RBI is not just deciding whether to move rates. It is deciding how much currency pain it is willing to absorb before policy itself has to change shape. For investors, that means the central bank’s next message matters almost as much as the decision. A pause may be read as stability, but in a shock like this it can also be read as quiet discomfort.

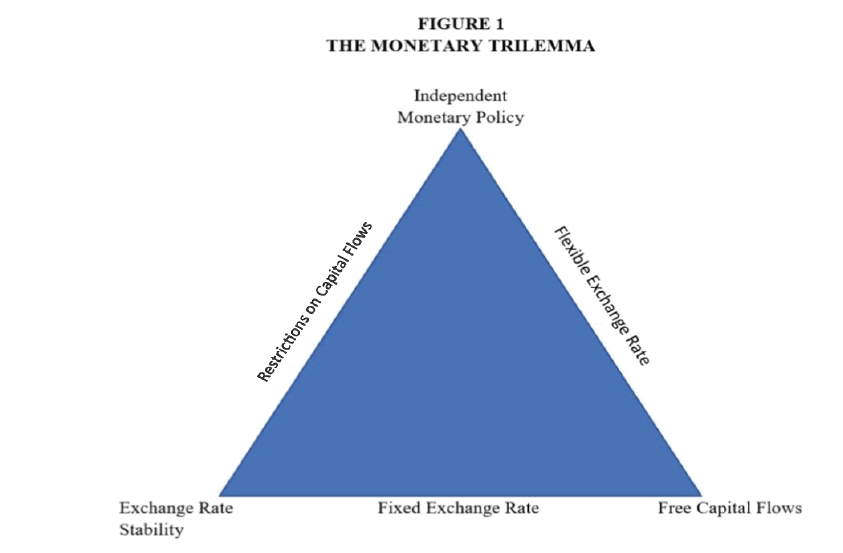

The impossible trinity is back

This week brings an old macro idea back into focus: the impossible trinity.

A country cannot fully have all three at once — free capital movement, a stable currency, and independent monetary policy. It can manage two. It cannot hold all three forever.

India has spent years trying to stretch that constraint. The rupee has been managed, the policy framework has stayed relatively independent, and capital flows have been increasingly open. The NDF ban says that stretch has limits. In stressful conditions, the RBI has chosen to reduce openness to protect the other two.

That is a major signal.

It tells us that rupee internationalisation is not a one-way road. It can advance in normal times and retreat in stress. It also tells us that emerging-market central banking is not just about rates and inflation forecasts. It is about boundaries: who gets access to the currency, how much volatility the system can take, and how far the central bank is willing to let the market test it before drawing a line. This week, the line was drawn.

Think of it like a gate on a crowded lane. For years, the lane was opening wider to handle more traffic. Last week, the gate closed because the traffic became the problem.

Who feels it first

These moves do not hit everyone in the same way.

Banks lose flexibility in treasury books and may take losses as positions unwind. Corporates lose easy hedging routes and face a more regulated FX market. Import-heavy businesses feel the rupee in their input costs. Oil marketing companies become the quiet shock absorbers if fuel prices are not passed through. Consumers see the effect last, but they are not spared. They just pay later, through prices rather than headlines.

That distribution matters for investors.

A weak rupee is not one story. It is several stories moving at different speeds. Urban consumers feel it in travel, electronics, and discretionary imports. MSMEs feel it in raw materials and inventory costs. Remittance-linked households feel it through global labour market stress. The state feels it through the politics of fuel pricing. The macro story only looks simple from far away. Up close, it is uneven and messy.

That is also why sectors matter here. Banks, OMCs, import-heavy manufacturers, travel-linked consumption, and companies with dollar liabilities will feel this differently. The market will not move as one block. It will sort winners and losers by balance sheet exposure.

What the obvious narrative misses

The obvious story says the RBI defended the rupee.

The better story says India has, once again, run into the cost of trying to combine currency openness, monetary autonomy, and exchange-rate stability. The NDF crackdown is not just a technical move. It is a policy confession. It says that when stress arrives, financial openness may be the first thing sacrificed.

That is not a small point for long-term investors.

A country that wants a globally used currency has to tolerate more market depth, more volatility, and more foreign participation. A country that wants tight control during stress has to accept that integration will move in fits and starts. India is trying to do both. Last week showed where the pressure point is.

There is also a historical rhyme here. China faced a similar tension in 2015, when currency defence and capital freedom stopped pulling in the same direction. India is not China, and the institutional setup is very different. But the logic is familiar: when a currency starts to look like a one-way bet, controls become the default response. Pressure creates closure. Closure changes the market.

The investor takeaway

The main lesson is not that the RBI is panicking. It is that the RBI is choosing.

It is choosing currency stability over market openness. It is choosing to stop a disorderly move now, even if that means making rupee internationalisation harder later. It is choosing to manage the boundary, not just the exchange rate.

For investors, that means three things.

First, do not treat the rupee bounce as the end of the story. The policy response has changed the market structure, but it has not removed the underlying external pressure.

Second, watch inflation with a lag. The calm CPI number is not the shock itself; it is the pre-shock reading.

Third, pay attention to who carries the pain. Banks, OMCs, importers, and dollar-sensitive businesses will tell you more than the headline index will.

The RBI did defend the rupee. But it also revealed the price of defending it. That is the part worth remembering.

The market saw a rally. The system saw a boundary.

Disclaimer: I am not a registered SEBI Research Analyst and anything in the above article should not be construed as a recommendation. This should be read solely for education purposes.