Why India’s chip push is not about beating NVIDIA — and why that may be its greatest strength

For decades, India’s semiconductor story was a footnote.

Occasionally hopeful. Frequently embarrassing. Almost always unfinished.

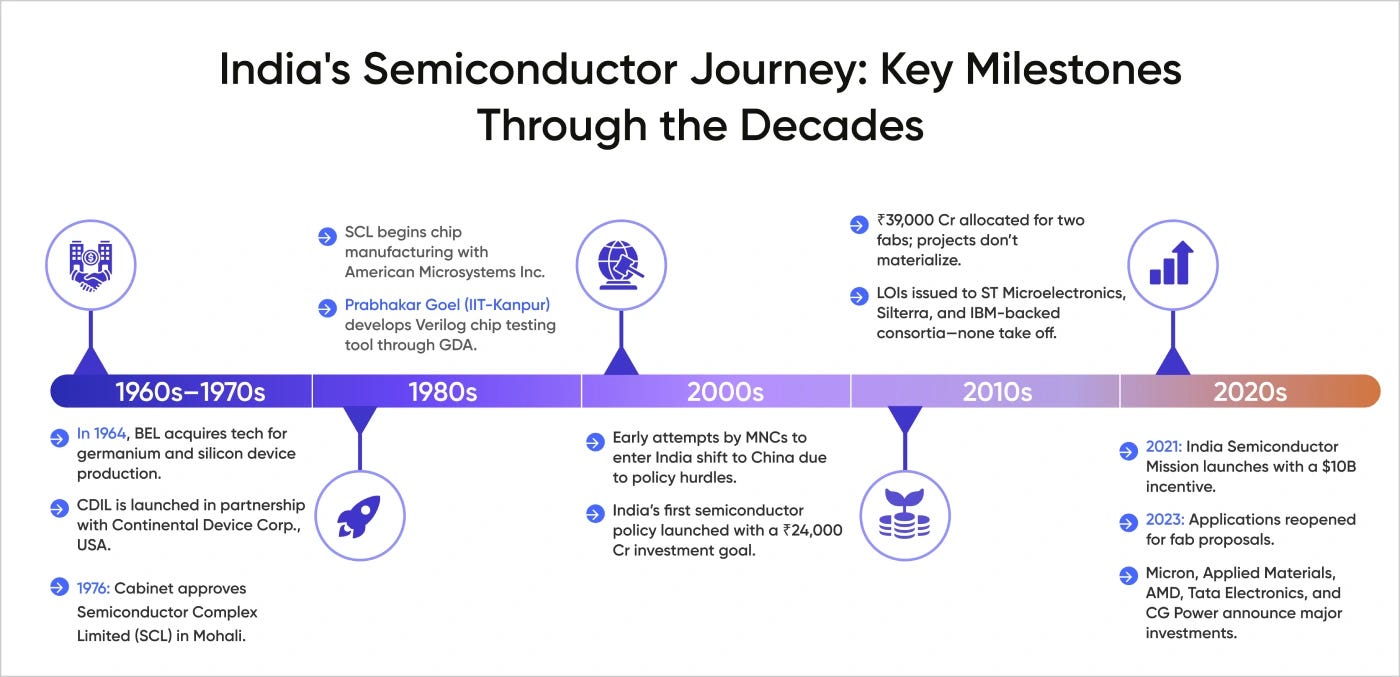

In the 1970s and early 1980s, India had early computing labs, public-sector electronics firms, and even indigenous hardware ambitions. Then the world moved. Taiwan built foundries. Japan mastered memory. Korea integrated vertically. The United States doubled down on design and tools. China poured capital into scale.

India, meanwhile, let the ball drop.

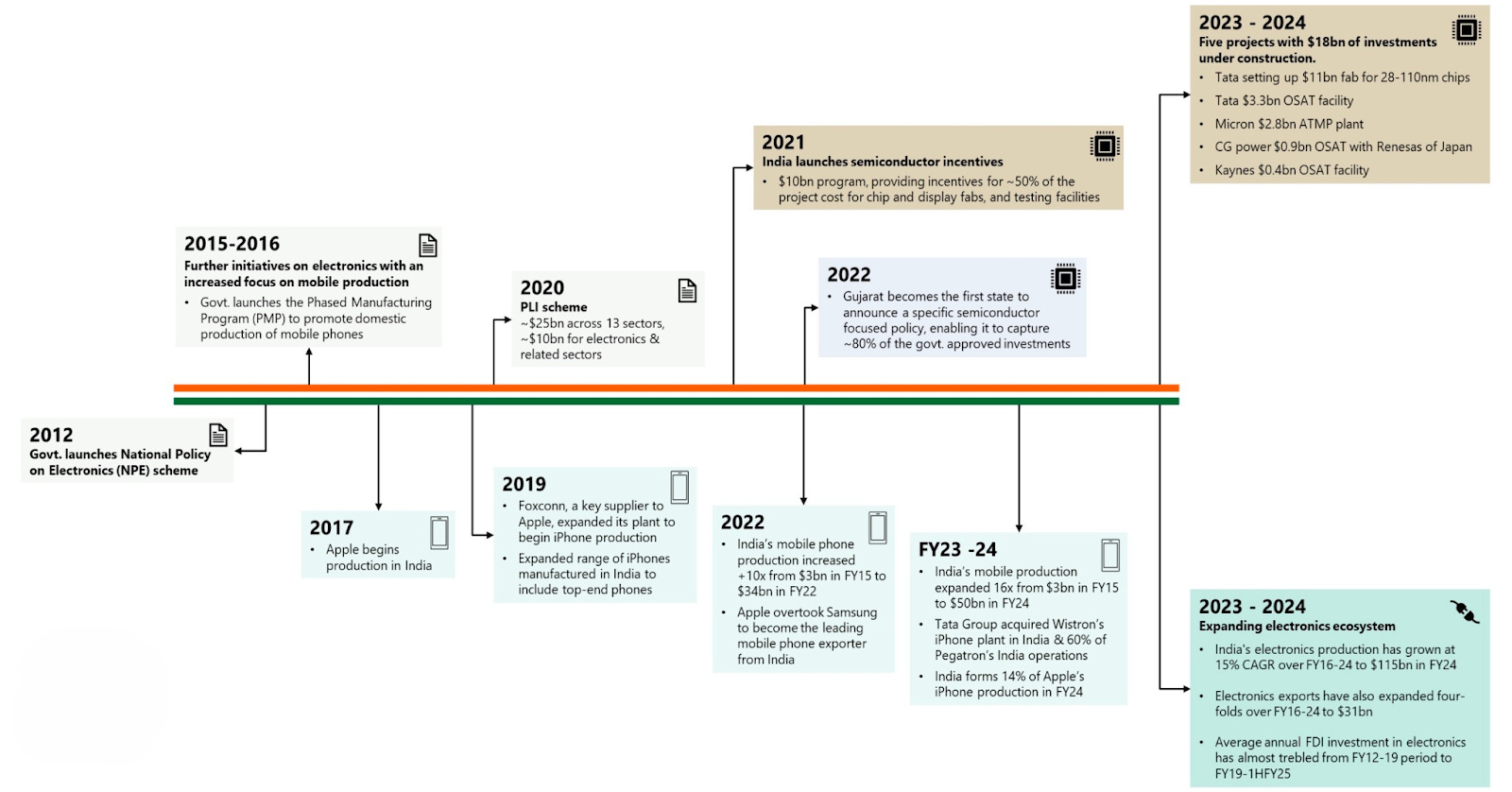

So when India announced the India Semiconductor Mission (ISM) in December 2021 with a $10-billion outlay, skepticism was not cynical — it was rational. The question wasn’t whether India wanted semiconductors. It was whether India could finally execute, stay the course, and build trust in an industry where credibility compounds slowly and collapses instantly.

Four years later, the answer is no longer theoretical.

India has crossed its first and hardest hurdle.

The next one will decide everything.

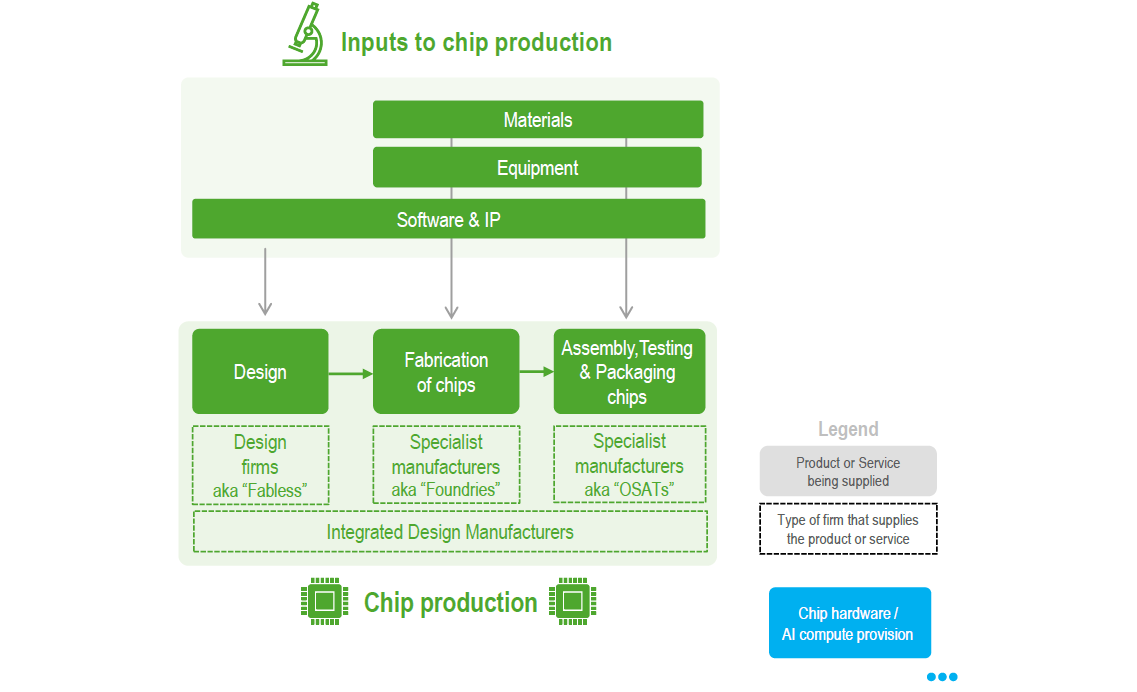

Why semiconductors are different from every other industrial bet

Semiconductors are not steel plants.

They are not smartphone factories.

They are not even electronics manufacturing services (EMS).

Semiconductors are ecosystems masquerading as factories.

A fab without suppliers bleeds money.

An OSAT without customers dies quietly.

A design ecosystem without downstream adoption becomes an outsourcing arm.

Every successful semiconductor nation learned this the hard way.

That is why India’s past attempts failed. Not because of talent shortages or lack of capital — but because the ecosystem logic was missing.

ISM 2021 quietly fixed that.

What actually changed in December 2021

The biggest shift was not money.

It was ownership.

Semiconductors moved from being:

This matters because semiconductors sit at the intersection of:

- geopolitics

- trade

- national security

- long-cycle capital

- global trust

Policy churn kills fabs. Political ambiguity scares suppliers. ISM’s mission-mode structure, permanent institutional memory, and external techno-financial vetting corrected for India’s historic weaknesses.

That’s why — for the first time — global players showed up with balance sheets, not PowerPoints.

The first hurdle: capacity creation (India cleared it)

Between 2021 and 2025, India did something many thought impossible:

- Secured 10+ real semiconductor projects across:

- ATMP / OSAT

- silicon and silicon-carbide fabs

- logic and power semiconductors

- Attracted firms like Micron, Tata Electronics, PSMC, CG Power, Kaynes

- Committed up to 50% capex support, with states adding another 20–30%

- Built electronics manufacturing scale that now rivals global hubs

Electronics production rose from ₹1.9 lakh crore (FY15) to ₹11.3 lakh crore (FY25).

Mobile phone exports jumped 127× in a decade.

Electronics exports crossed ₹3.3 lakh crore.

These are not cosmetic numbers.

They are the demand gravity that makes semiconductor investments rational.

By 2030, India is expected to consume $110 billion worth of semiconductors — nearly 10% of global demand. India already represents ~10% of real consumption, even if sales are booked elsewhere.

This is why fabs came.

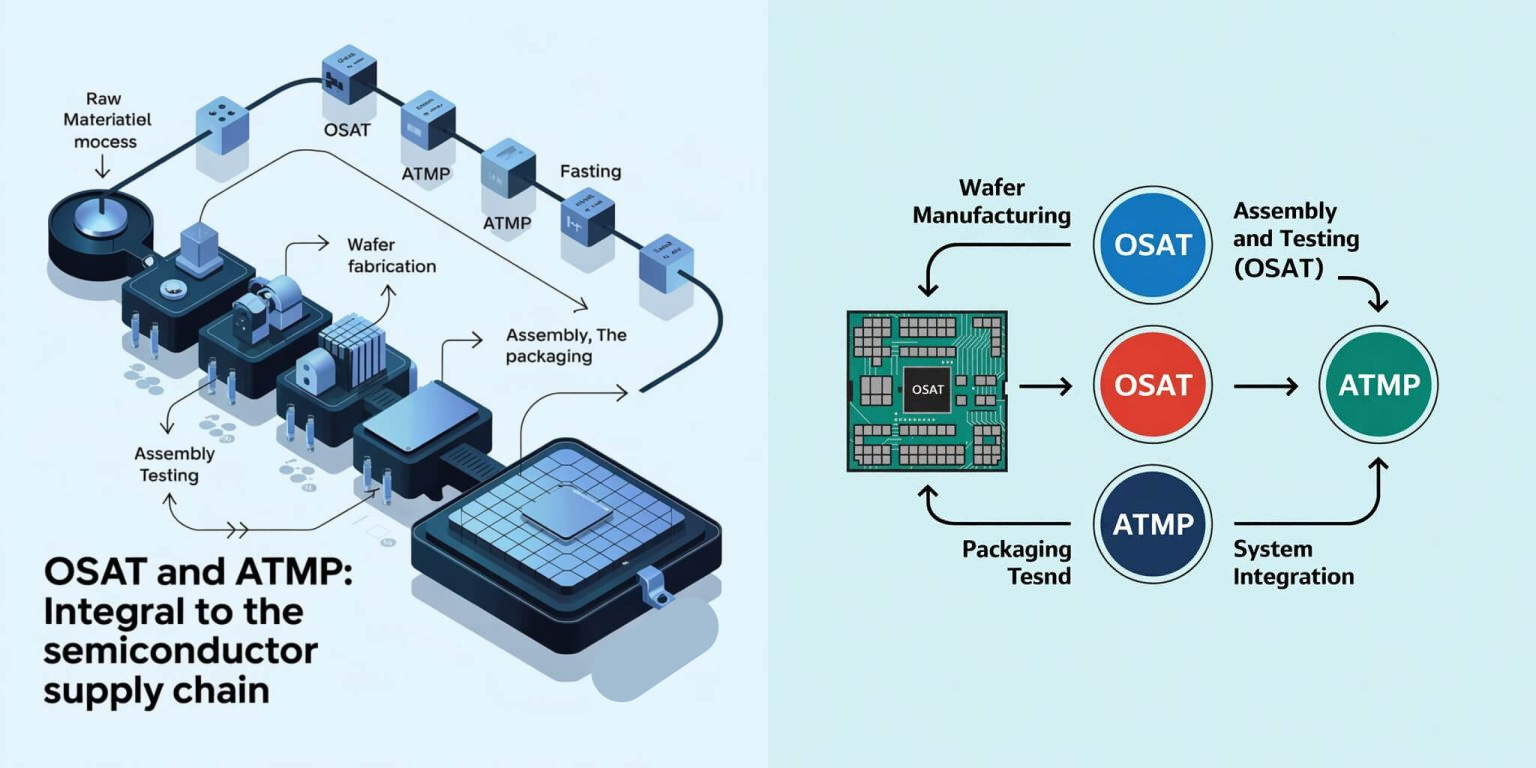

Why India started with packaging — and why that was the right call

Critics love to mock India’s early focus on assembly, testing, and packaging (ATP / OSAT) as “low value.”

This is a misunderstanding of how semiconductor ecosystems actually form.

Globally, 75% of ATP capacity sits in Asia, concentrated in China and Taiwan. It is capital-lighter than fabs but operationally brutal — yields, uptime, logistics, and quality discipline matter more than press releases.

Micron’s ATMP plant in Gujarat is not symbolic.

It is a trust anchor.

Once OSATs operate at scale:

- suppliers begin to localize

- OEMs test downstream integration

- learning curves move onshore

Every successful semiconductor hub — Taiwan, Malaysia, even China — entered through this door.

India is doing the same.

The second hurdle: utilisation (this is where countries fail)

Capacity is necessary.

Utilisation is survival.

This is where the story becomes uncomfortable — and honest.

As OSAT facilities come online in 2026–27 and fabs follow around 2028–29, India faces a make-or-break challenge:

Who will buy these chips?

OSATs do not live off startups.

They live off OEMs — automotive, industrial, telecom, consumer electronics.

If OEM manufacturing remains in:

- China

- Vietnam

- Thailand

then Indian OSATs become export service providers, not ecosystem anchors.

Margins stay thin. Supply chains stay imported. Subsidies never end.

This is why ISM 2.0’s real battle is not fabs.

It is downstream demand creation.

The missing middle: India’s biggest structural gap

One expert put it bluntly:

India has chip designers at one end, and 1.4 billion consumers at the other. Everything in between is missing.

India has:

- world-class chip design engineers (~20% of global pool)

- massive demand in autos, phones, appliances, networks

What it lacks:

- Indian fabless product companies at scale

- Indian OEMs defining silicon specs

- system companies absorbing early risk

This “middle layer” is what turns fabs into ecosystems.

Taiwan had MediaTek before TSMC scaled.

Korea had Samsung products alongside Samsung fabs.

China had Huawei, Xiaomi, BYD feeding SMIC.

India needs its own version — not replicas, but product-first companies that pull silicon through the system.

Why India is not trying to beat NVIDIA (and shouldn’t)

At this point, many readers ask:

Where does this leave AI chips, GPUs, and NVIDIA?

Here’s the uncomfortable truth:

India is not in NVIDIA’s game — and that is intentional.

As NVIDIA’s CEO famously framed it, this is no longer a data center game. It is an AI factory game — trillion-dollar infrastructure bets, vertically integrated stacks, and physics-limited roadmaps.

India is not building AI factories.

India is positioning itself inside the global AI supply chain.

That distinction matters.

India’s play is horizontal:

- materials

- chemicals

- equipment

- design IP

- packaging

- system integration

These layers:

- outlast chip cycles

- survive price wars

- embed nations permanently into global stacks

Trying to build a GPU rival today would be symbolic suicide.

Building indispensability is strategic realism.

Why ISM 2.0 matters more than ISM 1.0

ISM 1.0 solved credibility and capacity.

ISM 2.0 targets what actually determines success:

- upstream suppliers (chemicals, gases, equipment)

- downstream OEM manufacturing

- fabless IP ownership

- EDA cost barriers

- patient capital

One uncomfortable insight from the field:

Without chemical localisation, India cannot be globally cost competitive — subsidies or not.

Epoxies, plating chemicals, molding compounds, specialty additives — these decide OSAT margins. India’s chemical industry gives it a fighting chance here, if policy execution matches ambition.

Compound semiconductors: India’s asymmetric opportunity

If there is one domain where India could leapfrog quietly, it is compound semiconductors:

- silicon carbide (SiC)

- gallium nitride (GaN)

These power:

- EVs

- fast chargers

- renewable grids

- 5G RF systems

They care less about transistor scaling and more about:

- materials science

- power efficiency

- manufacturing discipline

This aligns naturally with India’s strengths in:

- chemistry

- power electronics

- automotive demand

- energy transition

This is not headline territory — but it is where durable value hides.

Capital: the silent constraint

Semiconductor startups do not fit venture capital timelines.

They need:

- 10–15 year horizons

- patient capital

- early buyers

- government as risk-absorber, not micromanager

Without fixing this:

- startups stall at prototype stage

- design talent migrates back to multinationals

- fabs lack domestic customers

This is why structural policy fixes matter more than incentive announcements.

What success actually looks like by 2030

India will not “win” semiconductors by shipping a 3-nanometer chip.

India succeeds if:

- OSAT utilisation stays high without perpetual subsidies

- OEM manufacturing meaningfully shifts onshore

- key materials and chemicals localize

- Indian fabless firms design chips that actually ship

- a second wave of fabs commits with lower incentives

- policy remains boring, predictable, and consistent

That is how ecosystems become irreversible.

The real story so far

India’s semiconductor mission is not a sprint.

It is not a race with Taiwan, Korea, or the US.

It is not a vanity project to match NVIDIA slide for slide.

It is something rarer and harder:

A deliberate attempt to make India impossible to exclude from the future of electronics and AI.

The first hurdle — capacity — is behind us.

The second — utilisation, supply chains, and customers — will decide the legacy.

And for the first time in decades, India has a credible shot at clearing it.

Not loudly.

But permanently.