Don’t fall for it

The financial world is currently obsessed with a single question: What is your FIRE number?

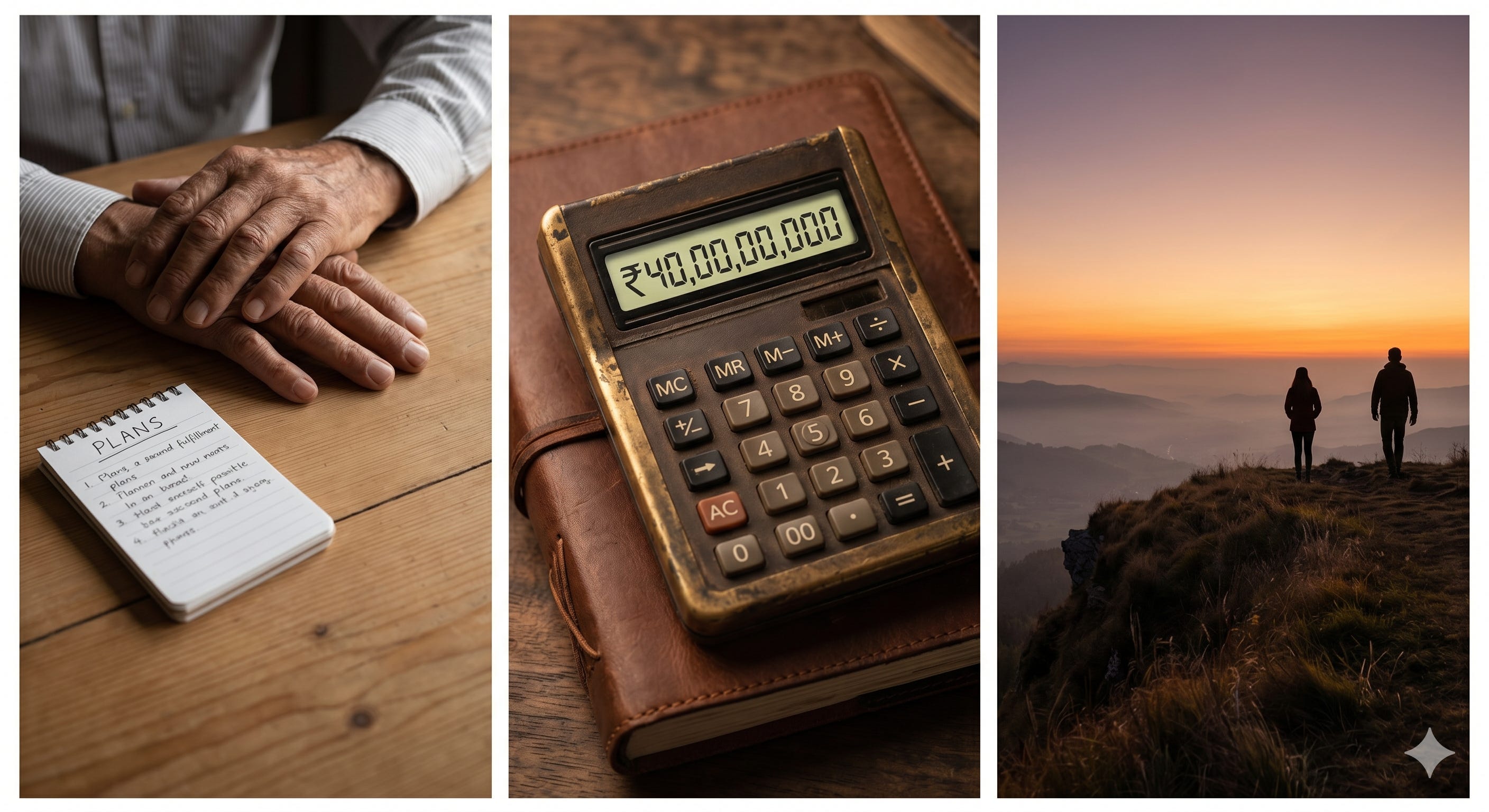

Recently, Dezerv founder Sandeep Jethwani sparked a viral debate by suggesting a retirement corpus of ₹40 crores. To be fair, he had a very specific persona in mind: a 40-year-old spending ₹2 lakhs a month, desiring global travel and elite club memberships, planning to retire at 60 and live until 90.

But look closely at that calculation and you’ll see a mountain of “ifs.” If you live in a Tier-1 city; if you want luxury vacations; if your inflation estimates are exactly $x$%; if your life expectancy hits 90. The reality is that a FIRE number cannot be generalized. It is a deeply personal variable shaped by current lifestyle, future aspirations, and geographical costs.

However, the problem with FIRE isn’t just the math—it’s the logic.

The Circular Reference Error

Calculating a FIRE number is essentially a circular referencing error in an Excel sheet. The goal of “Retire Early” is to quit as soon as you hit your number. But to calculate that number, wealth managers ask you to fix a retirement age (say, 50 or 60).

If you fix the age, you lose the essence of “retiring early” based on wealth. If you don’t fix the age, you can’t calculate the corpus needed to sustain the unknown years remaining. You are trying to solve for two variables in the same equation—the “when” and the “how much”—without fixing either. It’s a financial paradox that often leads to “One More Year” syndrome, where you keep moving the goalpost and never actually leave the field.

FI vs. RE: A Tale of Two Definitions

We need to decouple Financial Independence (FI) from Retire Early (RE).

Most people chasing FIRE aren’t actually looking for a permanent vacation; they are looking for an “Exit Strategy” from a toxic job or a soul-crushing routine. They want the freedom to pursue a hobby or start a business.

But let’s be honest: if you quit your job to start a consultancy or a café, you haven’t retired. You’ve just pivoted. For this, you don’t need ₹40 crores; you need a “runway”—perhaps 2 to 3 years of expenses—and the confidence that you can rejoin the job market if the venture fails.

The “RE” part is even more complicated because retirement is an emotional state, not just a financial one. I think of my grandfather, who retired at 60 after 42 years in a government job. Work was his hobby. When he finally had the financial independence to sit back, he felt uneasy. He had no other routine. If you spend your entire life chasing a number, you might find that once you reach it, you’ve forgotten how to live without the chase.

The Wealth Manager’s Fear Factory

There is a predatory element to these massive numbers. Telling a 30-year-old earning ₹1 lakh a month that they need ₹20 or ₹40 crores to retire is mathematically intimidating. When a wealth manager suggests you need to invest ₹80k a month to reach that goal—while your take-home pay barely covers rent—they aren’t giving you a roadmap; they are instilling fear.

That fear drives you toward complex products and advisory fees. Anyone can run numbers on an Excel sheet, but the wealth manager doesn’t have to live your restricted life while you’re trying to fund that massive corpus. They just collect the fee.

A Simpler Path to Sorted Finances

When I left my corporate job 1.5 years ago, I didn’t have a “FIRE number.” I had about a year’s worth of expenses and a decade of disciplined investing behind me. I knew it wasn’t enough to never work again, but it was enough to try something of my own.

If you want to be “sorted” without the existential dread of a ₹40 crore target, follow these simple principles:

- The 40-50% Rule: Aim to save and invest 40-50% of your monthly take-home pay. This includes EMIs for education or housing, as these build assets. Avoid EMIs for lifestyle liabilities.

- Dynamic Asset Allocation: Focus on a solid mix of equities, gold, and debt that evolves with your risk profile.

- The Two-Year Runway: If you hate your job, don’t wait for “retirement.” Check if you have a solid idea and a two-year cash runway.

- Keep the “Backdoor” Open: Most startups (over 95%) fail. Don’t feel bad about it—just ensure your skills remain sharp enough to rejoin the job market if needed.

Don’t let a spreadsheet tell you when your life begins. Focus on the independence, stay disciplined with your savings, and keep working as long as it brings you value. Real “FIRE” isn’t about hitting a magic number; it’s about having enough to say “no” to things you hate and “yes” to the things you love.

And if you need a blueprint on what to do if you plan to take a “career break”, you can watch this video I made last year when I had just taken one.