You probably stopped refreshing the US-Iran war news a few weeks ago. The ceasefire announcements. The Hormuz updates. The diplomatic back-and-forth. They aren’t hitting headlines. People got bored. It all started to blur.

But here’s what didn’t stop: the price of building the nation and your house is still climbing. Quietly. Relentlessly. Not just cement and steel — but your floor tiles, AC copper pipes, electrical wiring, plumbing, plywood, and the glass in your windows.

There’s also a twist buried inside this story that most analysts are missing.

Read on!!

Construction is basically energy converted into infrastructure

The moment energy becomes expensive, every material built on top of it starts repricing. India is simultaneously building highways, metros, airports, factories, data centres, and millions of homes. That scale has enormous energy embedded in it — diesel for transport, petcoke for kilns, gas for furnaces, crude for polymers.

The IEA described the Hormuz disruption as “the greatest global energy security challenge in history.” What that means on the ground in India: a simultaneous cost squeeze across every single construction input category — not one or two, but all of them, at the same time.

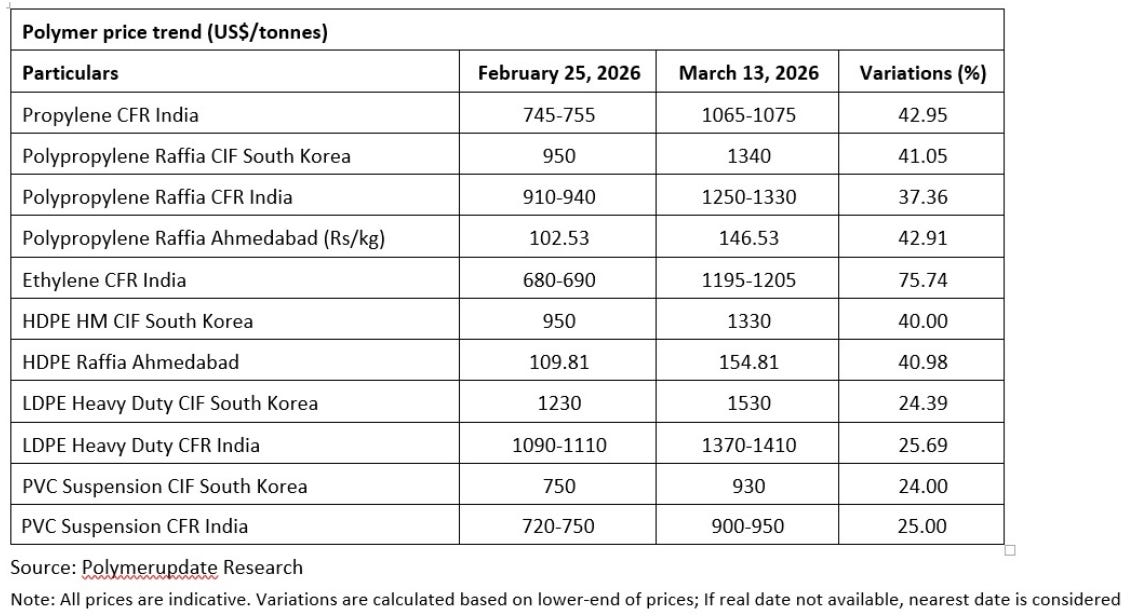

The cost shock is broad-based. Here’s the full bill

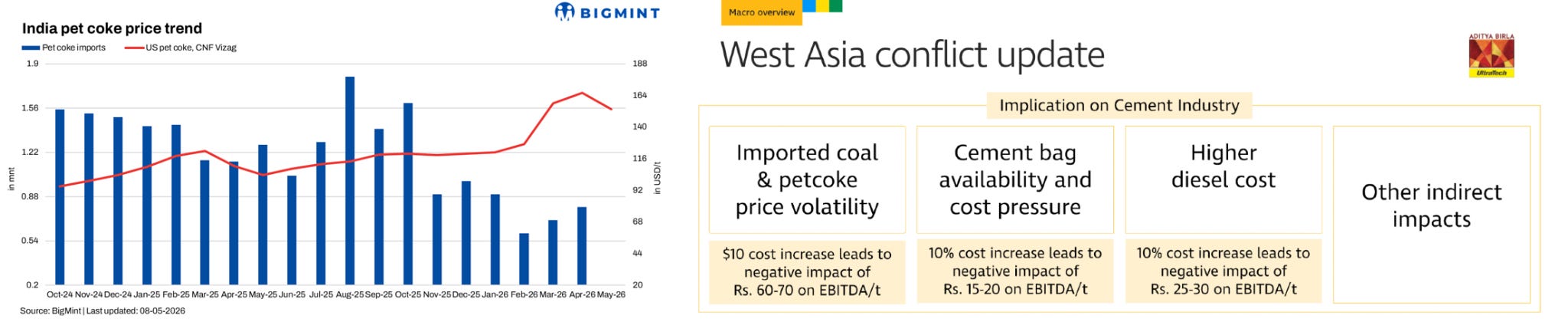

Cement. The industry burns imported petcoke to manufacture clinker. Petcoke prices jumped from ~$118 to ~$160 per tonne since the conflict. Kotak Institutional Equities flags a potential ₹300–400 per tonne margin hit in coming quarters. Cement companies are already switching to costlier domestic coal as a substitute. Price hikes to consumers are a matter of when, not if.

Steel. Queensland floods hit Australian coking coal in January; the Iran conflict worsened it. Capesize freight rates rose from $9.80 to $12.20 per tonne within weeks. Iranian iron ore pellet imports — nearly 1.88 million tonnes between April 2025 and February 2026 — are now at risk. The landed cost increase is adding roughly ₹50 per square foot to Mumbai high-rise construction.

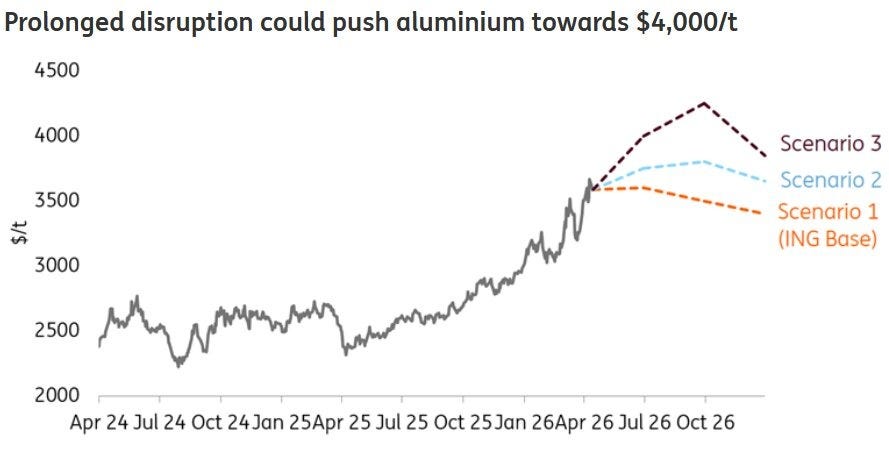

Aluminium. The Gulf accounts for 8–9% of global output. Alba (Bahrain) declared force majeure; Qatar’s Qatalum moved to restricted shutdown. Global prices crossed $3,400 per tonne. Indian producers — Nalco, Hindalco, Vedanta — face a double bind: higher output prices, but their CPC imports from the same disrupted region cost more too.

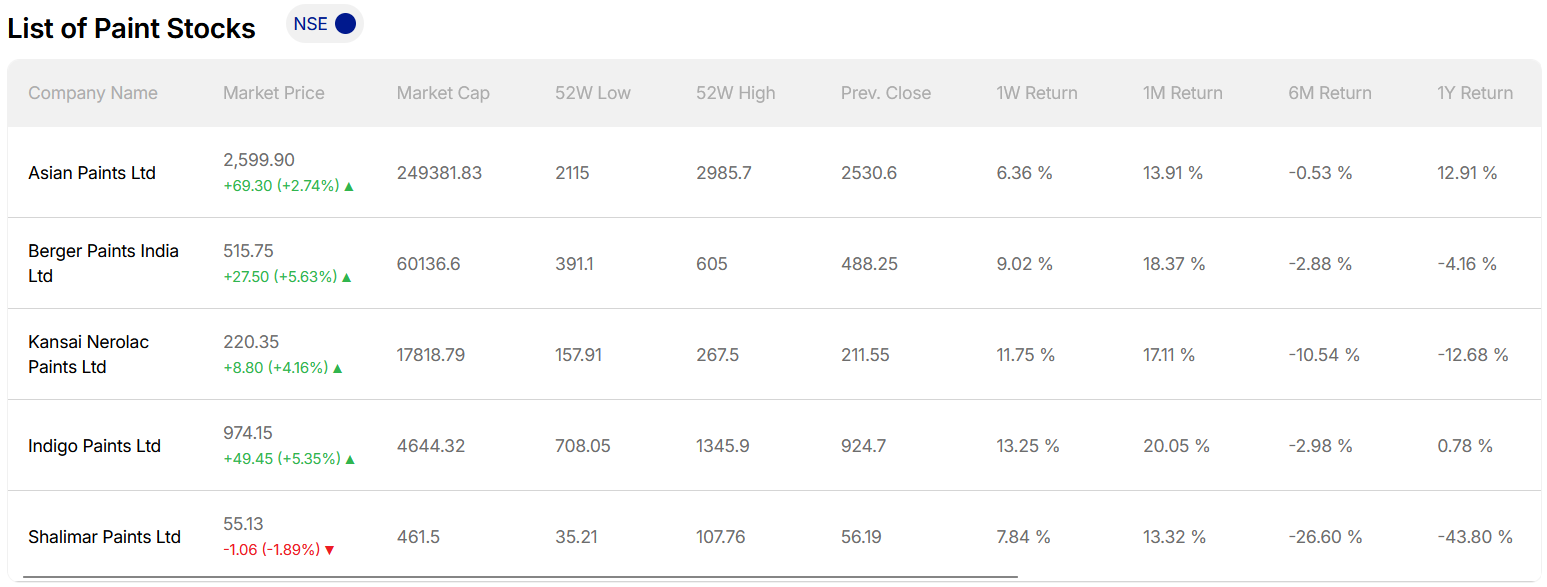

Paints. 55% of raw materials are crude-oil derivatives. Every $1 rise in crude cuts EBITDA margins by 0.25%. Asian Paints and Berger have initiated calibrated hikes, with 5–10% price increases expected in Q1 FY27 — colliding with softening demand and 50–60x earnings multiples that assumed steady growth.

PVC, plumbing, and bath fittings. PVC is ethylene-based — crude is its feedstock. Reliance Industries and Chemplast implemented hikes of up to ₹6,000 per metric tonne in March 2026. PVC resin prices have moved from ₹85–95 per kg to ₹100–120 per kg. Every drainage pipe, CPVC hot-water line, and conduit in your walls runs through this chain. Morbi’s sanitaryware division has announced 15–20% price hikes on taps, showerheads, and fittings. A bathroom that cost ₹2.5 lakh to finish six months ago now costs closer to ₹2.9–3 lakh — before any tile upgrade.

The one nobody saw coming: Your AC and your wiring.

It’s peak summer. Delhi-NCR logged 42–45°C in late April. Every Indian middle-class family is either buying an AC or running one harder than ever.

AC manufacturing depends on gas to braze the copper pipes that carry refrigerant. When Iran’s retaliation disrupted QatarEnergy-linked gas supplies, those brazing gases became scarce. India’s top AC makers — Voltas, Daikin, LG, Haier, Blue Star — had already pushed 7–9% cumulative hikes until March. Then came another 7.5–12% hike from April 1, directly triggered by the war. A 1.5-tonne split AC this summer costs ₹4,000–7,000 more than it did in January.

For construction, the copper story runs deeper. Copper wire prices surged 20.7% in February 2026 alone. At ₹500–700 per kilogram and rising, every 10% copper increase pushes finished cable prices 4–5% higher. A standard 2BHK electrical setup costs ₹46,000–72,000 — up 8–12% in 2026. A 3BHK with dedicated AC circuits and MCBs approaches ₹1,00,000. Distribution boards and surge protection are moving in the same direction.

The last mile: Sand, bricks, plywood, and glass.

These are the inputs nobody thinks about until a contractor quote arrives.

Sand — river sand runs ₹4,500–8,500 per truck. Not Gulf-driven, but diesel-driven. Every transport cost increase is a quiet tax on volume. Bricks — fly ash bricks cost ₹6–9 per piece, red clay ₹7–12. Kiln energy and diesel freight are the swing variables; both are up.

Plywood is the skeleton of every modular kitchen, wardrobe, and fit-out. The resins binding it — urea formaldehyde, phenol formaldehyde — are petrochemical derivatives. BWR-grade plywood (kitchen-safe) now runs ₹65–100 per sq ft; marine grade reaches ₹210. A 3BHK interior fit-out consumes ₹1.2–2.5 lakh of plywood alone, before laminates or labour. Price spikes show up with a lag — but they compound across every room.

Glass and uPVC windows: uPVC is a crude derivative. Tempering glass requires furnaces running at 650–700°C — the same energy-cost logic as ceramic kilns. Mid-range windows with toughened glass now cost ₹450–900 per sq ft. Window and glazing costs for a 1,500 sq ft apartment can run ₹3–6 lakh — a number that has moved meaningfully in three months.

The most vivid example: A kiln in Morbi

Morbi, Gujarat — world’s second-largest ceramics cluster, 800 units, 90% of India’s ₹75,000 crore ceramics industry. Those kilns run at 1,200°C, 24 hours a day, on propane and piped gas sourced from Gulf routes. When propane collapsed, the cluster shut from March 17. Workers went home. When kilns restarted on piped gas in late April: standard tiles moved from ₹22 to ₹30 per sq ft; glazed vitrified tiles (most residential projects) up ₹7 per sq ft; sanitaryware up 15–20%.

That’s not inflation on a spreadsheet. That’s your bathroom. Your kitchen floor. Your possession handover quote.

The slow normalization is the real risk

Builders absorb costs first — raising apartment prices into softening demand is commercially painful. So margins compress, launches slow, contractors renegotiate, possession gets deferred. Eventually the market resets to a higher base price. This is how inflation enters real estate — gradually, then permanently.

The twist most analysts are missing

The same worker who was building towers in Dubai may now be back bidding on Indian highway and housing projects. Remittances to Kerala, Bihar, UP and Andhra Pradesh will feel pressure. But India’s construction sector has struggled with labour shortages for years — this returning pool arrives precisely when domestic infrastructure spending is accelerating. A partial self-correction nobody is pricing in.

And once the dust settles, Gulf reconstruction demand will be enormous. L&T, NBCC, Engineers India — all with proven Gulf credentials — are positioned for it. The crisis hurting margins today could create a reconstruction supercycle for Indian EPC companies tomorrow.

What to actually do?

- Buying? Prefer developers with strong balance sheets and near-completion inventory over leveraged builders promising ambitious launches.

- Renovating? Advance purchases in copper wiring, PVC, tiles, plywood, and modular components — these are the most globally exposed categories. Delays cost more.

- Investing? The winners will have pricing power, procurement discipline, and intact balance sheets when reconstruction demand arrives.

A war near Hormuz may not look connected to a wiring quote in Hyderabad, a delayed AC installation in Delhi, or a tile estimate in Pune that came in 25% higher than expected.

But somewhere between an oil tanker, a shuttered kiln in Morbi, a bag of cement, and an EMI statement — the world arrives at your front door.

Disclaimer: I am not a registered SEBI Research Analyst and anything in the above article should not be construed as a recommendation. This should be read solely for education purposes.