Physical or ETF or Mutual Fund or SGB or …

In one of my recent posts, I explored why gold may be on the brink of a historic revaluation – a move that could reset not just America’s balance sheet, but the global monetary order. But knowing the why is only half the story. The real question is: how can we as investors position ourselves to benefit?

I had promised in the post that I will be soon writing on various options one has to invest in Gold. So here it is…

Let’s break down the most practical ways to invest in gold, their pros and cons, and who they’re best suited for.

Why Gold Matters

Gold has always been regarded as a safe haven, the ultimate “last resort” asset. When confidence in a country’s currency weakens, investors often fall back on the US Dollar. But when even that stability comes into question, gold takes centre stage.

Its value is reinforced not only by its unique physical properties, i.e., malleability, non-reactivity, relatively low melting point, and natural lustre, but also by its scarcity. Nearly 80% of the world’s gold reserves have already been extracted, making the remaining supply increasingly precious and a key driver of rising prices.

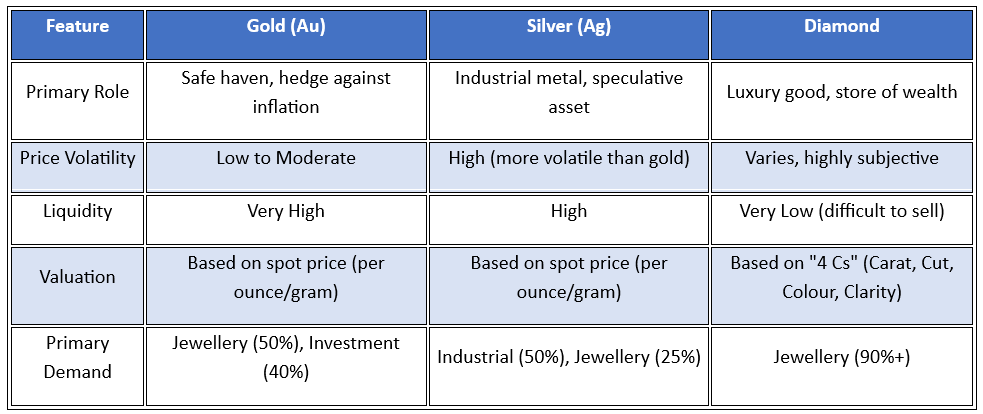

Comparison of Gold with Other Precious Metals

Gold Purity

- Karats measure purity; the highest is 24k, though true “100% purity” doesn’t exist.

- Coins and bars often use .995, .999, or .9999.

- 22k: most common for high-end jewellery.

- 18k: balances purity and hardness; ideal for designer pieces.

- 14k: more affordable, durable due to alloying.

Ways to Invest in Gold in India

1. The Classic Touch: Physical Gold

Jewellery:

This is the way our grandparents and parents did it, mostly the women in the family (your dadi, nani, mummy… or even your wife). There’s just something about holding a piece of your wealth in your hand.

- You get a beautiful piece to wear—great, but as an investment, it’s tricky.

- You’re paying for more than just the gold: “making charges” and a markup.

- It’s often a personal indulgence, not a financial strategy.

- Grandmother’s gold bangles—bought for beauty and legacy, not ROI.

Pros:

- Beautiful, wearable, sentimental value.

- Tangible asset you can touch.

Cons:

- Heavy premiums for “making charges” and design, usually lost at resale.

- Trust in jeweller is crucial for purity.

Charges:

- Making charges typically 10%-20%.

Bars & Coins:

The real deal for physical investors: buying pure gold with minimal extras, directly tied to market price.

Pros:

- Purest form of investment.

- Price is aligned with gold markets—clear and direct.

- No counterparty risk after possession.

Cons:

- Storage/security is a genuine headache.

- Need a secure safe or a bank locker (adds cost).

Charges:

- Making charges ~5% (can negotiate).

Taxation:

- 3% GST on both jewellery and bars/coins, applied on purchase price PLUS making charges.

- Up to 24 Months: Tax slab

- >24 Months: 12.5% LTCG

2. The Modern Approach: Digital Gold

Gold ETF:

Imagine a restaurant buffet (stock market). ETF is prepaid plate—you pay for exactly the gold you want, can buy/sell any time during market hours. Demat account required.

Pros:

- Instant, flexible, real-time prices.

- Excellent for active traders/investors.

Cons:

- Demat required.

- Brokerage + bid–ask spreads.

- Flexibility can tempt over-trading.

Charges:

- No STT, expense ratio ~0.5% to 1%.

Top ETFs:

- ICICI Prudential Gold ETF

- HDFC Gold ETF

- SBI Gold ETF

- Nippon India ETF Gold BEES

- Kotak Gold ETF

Taxation:

- Up to 12 Months: Tax slab

- >12 Months: 12.5%

Gold Mutual Fund:

Meal delivery subscription – chef (fund house) tracks gold price daily and delivers performance to your account.

Pros:

- No Demat needed, SIP friendly, ideal for tracking and long-term holding.

Cons:

- Slightly higher expense ratio.

- Can buy/sell only once a day at NAV.

Charges:

- 0.2% to 0.8% on average.

Taxation:

- Up to 24 Months: Tax slab

- >24 Months: 12.5%

Sovereign Gold Bonds (SGBs):

Government gold certificate – earn fixed interest (currently 2.5%/year) and tax-free capital gains at maturity (8 years).

- SGB scheme discontinued for fresh subscriptions; last issue in Feb 2024.

- Existing bonds remain valid and accrue interest.

- If SGBs were still open, they’d be a clear winner!

Digital Gold Platforms:

Apps like Paytm let you buy gold for even ₹1. User-friendly, but beware of fees and lack of deep regulations.

Pros:

- Very easy to start, buy in tiny amounts.

- Great for building a gold saving habit.

Cons:

- Higher commissions and fees than ETFs.

- Regulations less secure than other options.

Hidden Cost:

- Spread is typically 2–6% (diff between buy and sell price eats into returns).

- Example: Spot price ₹10,000/gram; buy at ₹10,300 (3% higher), sell at ₹9,700 (3% lower), so 6% round-trip cost.

Taxation:

- 3% GST

- Up to 24 Months: Tax slab

- >24 Months: 12.5%

3. The Adventurous Path: Other Options

Gold Futures:

Trading gold price prediction contracts. High risk, potential for big wins/losses—mostly for experienced traders.

Pros:

- Quick, high gain potential.

Cons:

- Highly leveraged, risk of losing all capital (and more).

- Not recommended for most investors.

Gold-Related Companies:

Buy shares in gold-linked companies (Muthoot, Manappuram, Senco, Kalyan, Rajesh Exports, D.P. Abhushan, Titan, Motison, etc). Gives you gold exposure and business returns.

Pros:

- Exposure to gold sector, possible dividends, added business growth.

Cons:

- Your returns depend on company performance, not just gold price.

Gold Allocation in Your Portfolio

The main objective: act as a hedge to your overall portfolio

Ideal allocation? 10–15% for most portfolios, enough for hedging without hurting overall gains.

Studies show going above 20% can lower returns.

Creative Micro-Investing Apps

How do they work?

- Every purchase is rounded up (₹73 coffee → paid ₹75, extra ₹2 saved).

- App collects these round-ups, pools and invests them in gold (digital gold or ETFs).

- You get fractional ownership, stored safely.

- Easiest way for young savers to automate gold investing via Jar, Spare8, Gullak, etc.

So, Which Gold Route Should You Choose?

- For traders/active investors: Gold ETF

- For long-term passive (who want to SIP): Gold Mutual Fund

- For convenience/micro-savings: Digital Gold Platforms

- For sentiment/family use: Physical Gold

- For income & safety: Sovereign Gold Bonds (if you hold them)

Bottom line:

For wealth-building today, Gold ETFs and Mutual Funds stand out as the smartest, most balanced choices.

Disclaimer: I am not a registered SEBI Research Analyst and anything in the above article should not be construed as a recommendation. This should be read solely for education purposes.