Which companies might benefit?

The cloud is not invisible, as they say. There’s a huge infrastructure behind that cloud. It is called Data Centers. As AI transforms from a digital trend into an industrial force, India’s windowless “intelligence factories” are becoming the new blue-chip infrastructure.

By locking in scarce power, strategic land, and advanced liquid cooling, this sector is shifting from niche real estate to a high-moat, utility-like powerhouse.

Read along to know more players into this sector, from the listed space.

Every technological revolution has a moment when gravity returns.

In the internet era, it was fiber.

In mobile, it was spectrum and towers.

In EVs, it was batteries and charging.

For artificial intelligence, gravity looks less glamorous: uninterrupted power, ultra-low latency, cooling at scale, land near connectivity hubs, and control over data.

The point where all of these forces converge is the data center.

A data center is not a warehouse for servers. It is an industrial plant for computation, a facility that converts electricity into intelligence, 24 hours a day, every day, without pause. If electricity is the new oil, data centers are the refineries. And if AI is the next industrial revolution, these windowless concrete buildings are its factories.

From Real Estate to Critical Infrastructure

For years, data centers were treated as a niche real-estate asset class: long leases, predictable tenants, stable yields. That framing worked when workloads were predictable.

AI broke it.

Traditional cloud usage is bursty – peaks during business hours, softens at night. AI workloads do not sleep. Training models, running inference, powering copilots, fraud detection, recommendation engines, computer vision – these run continuously.

That changes the requirements completely. Modern AI-driven data centers demand:

- Near-perfect uptime

- Extremely high compute density

- Power availability measured in hundreds of megawatts

- Cooling systems operating at the edge of physical limits

The shift is visible in hardware. Older facilities were designed for 5–10 kW per rack, air-cooled, predictable. AI accelerators like NVIDIA’s H100 changed the equation. Today, new facilities are being designed for 20–60 kW per rack, with liquid cooling moving from exception to norm.

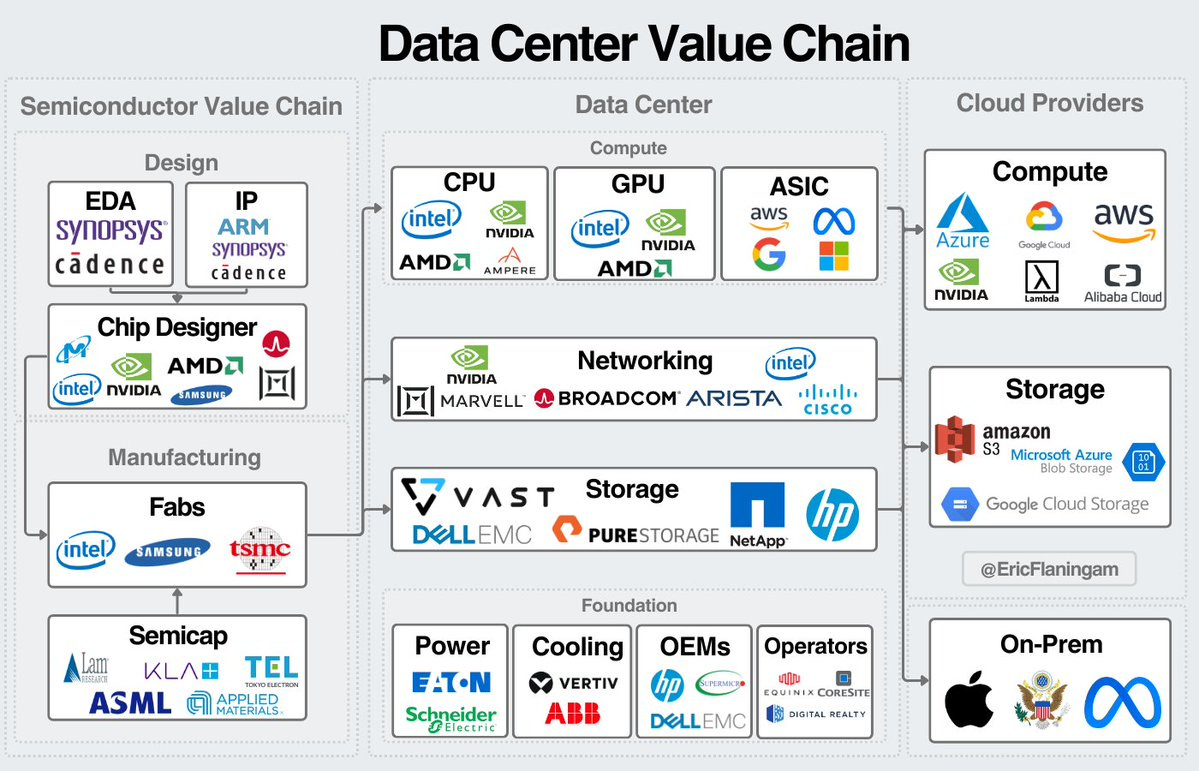

How the Data Center Market Actually Works

To understand where value accrues, the market needs to be unpacked properly. Data centers are classified along three axes: tenancy, reliability, and services.

Tenancy: Who Uses the Facility

- Enterprise data centers are captive facilities built by banks, governments, or large corporations for maximum control.

- Colocation data centers are shared facilities where operators provide space, power, cooling, and security, while tenants install their own hardware. This model allows enterprises to avoid heavy upfront capital expenditure and dominates most commercial deployments.

- Hyperscale data centers are purpose-built for cloud giants like Amazon Web Services, Microsoft Azure, and Google Cloud. These campuses are massive, power-intensive, and designed to serve millions of users simultaneously. This is where large-scale AI training happens.

India needs all three, but hyperscale capacity is what turns the country into a serious AI node.

Reliability: Why “Tier” Matters

The industry uses the Uptime Institute’s Tier framework:

- Tier I–II facilities offer basic redundancy and are increasingly unsuitable for mission-critical workloads.

- Tier III has become the commercial baseline, offering backup redundancy and high availability.

- Tier IV represents full fault tolerance and is growing fastest, driven by BFSI, healthcare, and real-time digital platforms that cannot afford downtime.

As AI workloads become business-critical, demand is steadily shifting up the reliability curve.

Services: Where Margins Differ

- Colocation offers stable, annuity-like returns.

- Managed services and disaster recovery offer higher margins but require deeper operational expertise and geographic dispersion.

Each layer has different risk-return characteristics, but all benefit from rising compute intensity.

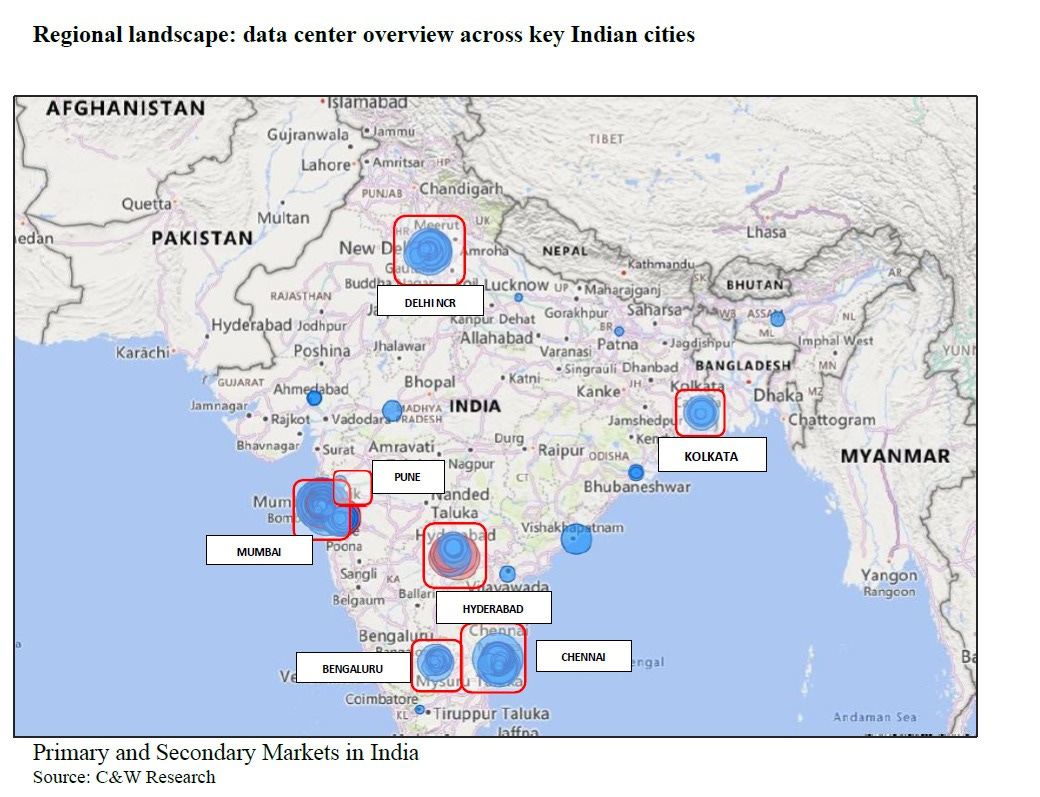

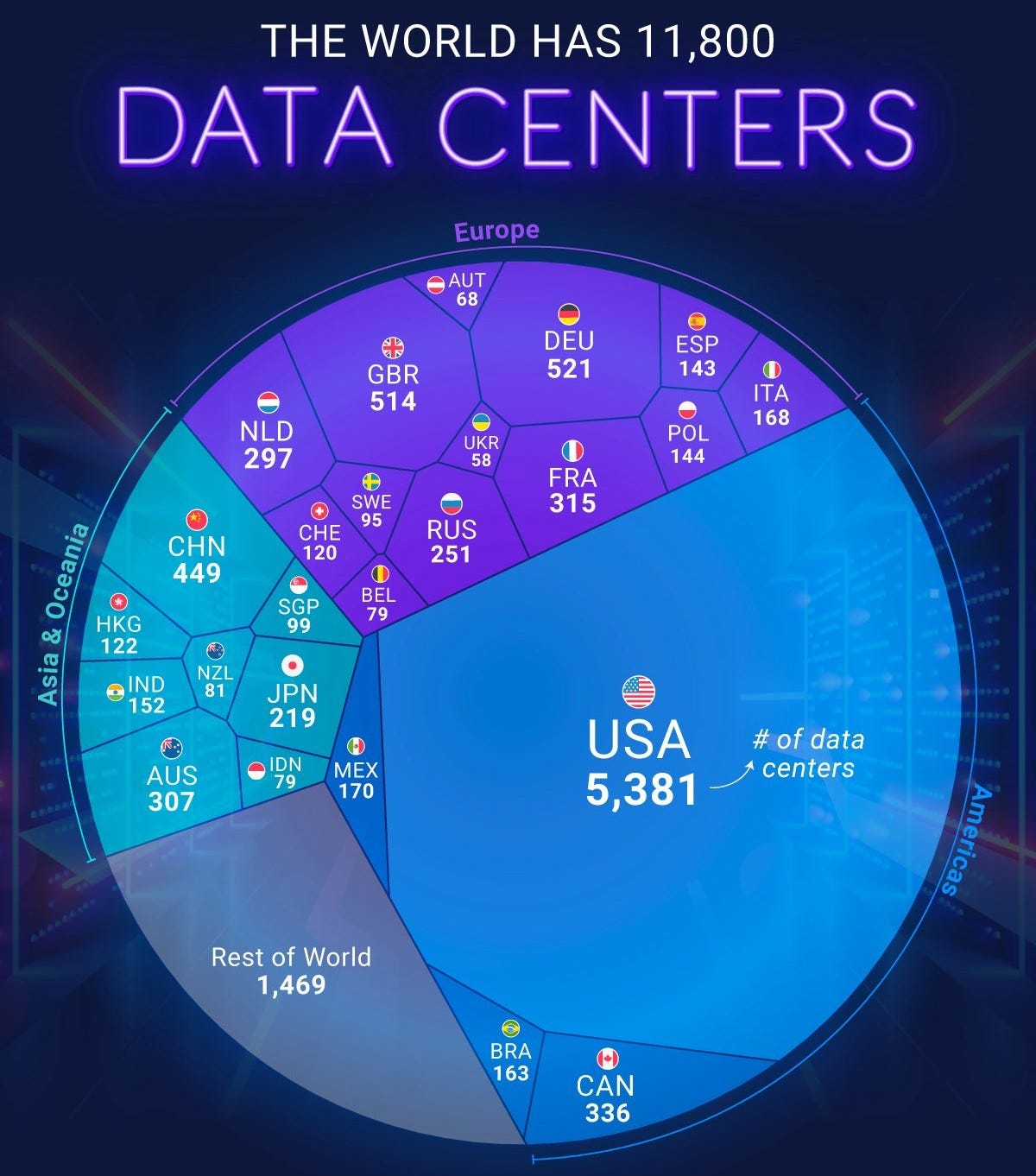

Why India Is Heating Up

India’s data center capacity has expanded rapidly over the last five years and is still early relative to demand. Most credible projections point to multi-gigawatt capacity addition over this decade, driven by a mix of regulation, demand, and infrastructure build-out.

Three forces matter most.

- Data localisation is no longer optional. Financial data, government platforms, and sensitive personal data are increasingly required to be stored and processed domestically. This creates non-discretionary demand.

- AI and cloud adoption are accelerating simultaneously. Public and private investment into AI compute GPUs, platforms, and applications directly translates into data center demand. You cannot subsidise AI without building the physical layer beneath it.

- Connectivity is improving. Expansion of submarine cable landings and domestic fiber networks around Mumbai, Chennai, and emerging tier-2 hubs is reducing latency and making India viable as a regional processing node, not just a consumption market.

Policy: Less Noise, More Certainty

Policy momentum is now backed by unprecedented capital scale. Adani Group plans up to $100 billion in green, AI-ready data centers by 2035, including a 1 GW JV with Google, while Reliance Industries has announced a ₹7 lakh crore Gujarat program anchored by a mega AI facility in Jamnagar. Amazon Web Services, Microsoft, and Google have pledged over $15 billion across Mumbai, Chennai, and Hyderabad. Foreign data center investors receive a 21-year tax holiday until 2047, with Prime Minister Narendra Modi positioning India as a global hub.

Big Capital Has Noticed.

Where the Investment Opportunity Really Lies

Data centers sit at the intersection of five critical inputs: power generation, transmission, land, capital, and execution. The same logic that built scale in ports and renewables applies here. Once built, these assets are hard to replicate and harder to displace.

This is not a one-stock story. It is a system.

Power and Transmission

Utilities benefit as data centers become anchor loads demanding exceptional reliability. Unlike factories, data centers cannot tolerate grid fluctuations.

Listed proxies:

- Power Grid Corporation of India

- Adani Energy Solutions

- Tata Power

Industrial Real Estate

Land near connectivity hubs with sanctioned power and fiber access becomes strategic.

Listed proxies:

- Anant Raj Limited

- DLF

Cooling, Thermal & Electrical Equipment

Higher rack densities force redesign of cooling and power distribution.

Listed proxies:

- Schneider Electric Infrastructure

- Blue Star

- Yash Highvoltage

- Aeroflex Industries

- KRN Heat Exchanger and Refrigeration

Specialized EPC & Integration

Mission-critical buildouts require experienced engineering and integration capabilities.

Listed proxies:

- Larsen & Toubro

- Techno Electric & Engineering Company

- KEC International

- Black Box

Fiber and Connectivity

Submarine cable landings and dark fiber networks form the backbone between clusters.

Listed proxies:

- Sterlite Technologies

- HFCL

- Bharti Airtel

- Tata Communications

Servers, HPC & Cloud Platforms

Compute hardware and cloud infrastructure scale with AI and data center expansion.

Listed proxies:

- Netweb Technologies India

- Aurionpro Solutions

- E2E Networks

Conclusion

We spend our lives in the digital world, but rarely touch its physical form. Data centers are designed to be invisible.

For the next decade, they will be anything but.

AI’s compute hunger, India’s localization push, improving connectivity, and the entry of serious capital are converging into a durable infrastructure cycle. The challenges—power, cooling, land, talent—are real, but they are exactly what separates transient capacity from lasting assets.

The companies that lock in power, secure land, master high-density cooling, and navigate regulation will build infrastructure that compounds quietly for decades.

The factories of intelligence are being built now.

And like all great industrial booms, the real story is not the software on top but the concrete underneath.

Disclaimer: I am not a registered SEBI Research Analyst and anything in the above article should not be construed as a recommendation. This should be read solely for education purposes.