How Nuclear, Materials, and Fuel Cycles Are Quietly Rewriting the Global Power Order

In Part 1, we traced how the energy transition runs into hard limits once systems meet scale.

This is where those limits stop being theoretical and start shaping outcomes.

Once intermittency, material intensity, and system reliability are taken seriously, the focus shifts away from slogans and toward inputs: fuel, construction capacity, and control over time-dependent power. This is the less visible layer of the transition, but it is the one now setting direction.

IX. Uranium Is Not a Commodity — It Is a Strategic Relationship

If oil is traded, uranium is allocated.

This distinction matters more than most people realise.

Unlike coal, gas, or even copper, uranium does not move freely through global markets. It is bound by:

- international safeguards,

- bilateral agreements,

- traceability requirements,

- and long-term contracts that often run decades.

Utilities do not “shop around” for uranium during shortages. They lock in supply years in advance because reactors cannot simply switch fuels without regulatory and technical consequences. This turns uranium into something closer to critical infrastructure input than a commodity.

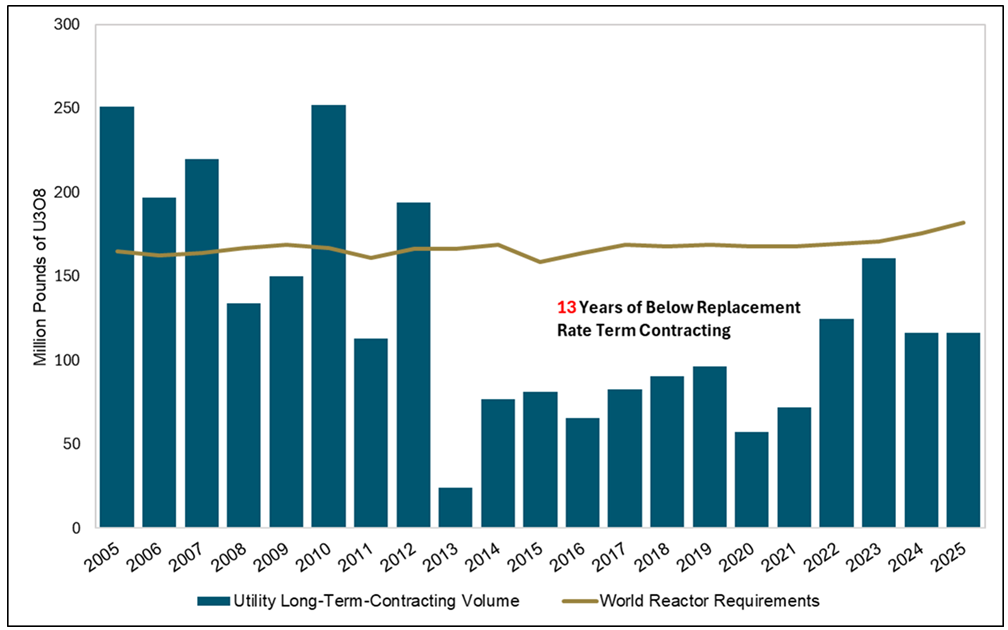

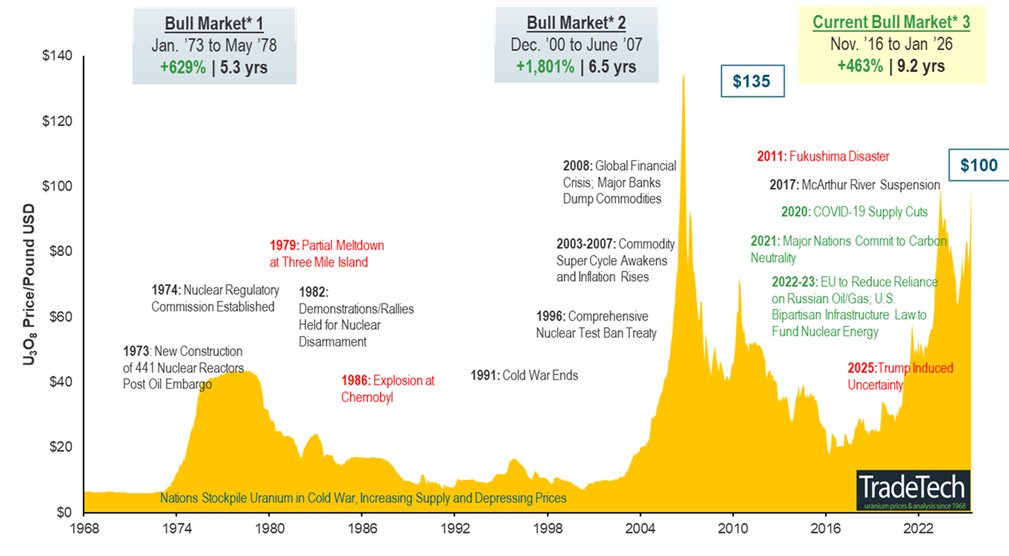

That is why the global uranium market behaves differently:

- prices move slowly, then violently,

- supply responds over decades, not quarters,

- and geopolitics matter more than spot economics.

This is the context in which India’s recent uranium diplomacy must be understood.

X. India and Canada: Why This Deal Is Bigger Than $3 Billion

India’s proposed long-term uranium agreement with Canada is often described as a supply deal. That understates its significance.

India’s domestic uranium production remains structurally insufficient. Its reserves are largely low-grade, meaning:

- more ore must be processed per unit of fuel,

- energy and water use rise,

- and reliability becomes harder to guarantee at scale.

At the same time, India’s reactor fleet is evolving. Indigenous heavy-water reactors can operate on natural uranium, but imported light-water designs require enriched fuel that India does not produce at scale for civilian use.

Canada solves both problems at once.

Canadian uranium is:

- among the highest-grade in the world,

- extracted with fewer processing steps,

- and produced in a politically stable, trusted jurisdiction.

The deal therefore secures not just volume, but quality and reliability over decades.

More importantly, uranium markets do not tolerate ad-hoc buying. Long-term contracts signal trust, alignment, and strategic intent. After years of strained diplomatic relations, both countries are effectively acknowledging that energy security overrides political turbulence.

For India, this is about buying time – time to expand reactors, stabilise grids, and develop next-generation fuel cycles.

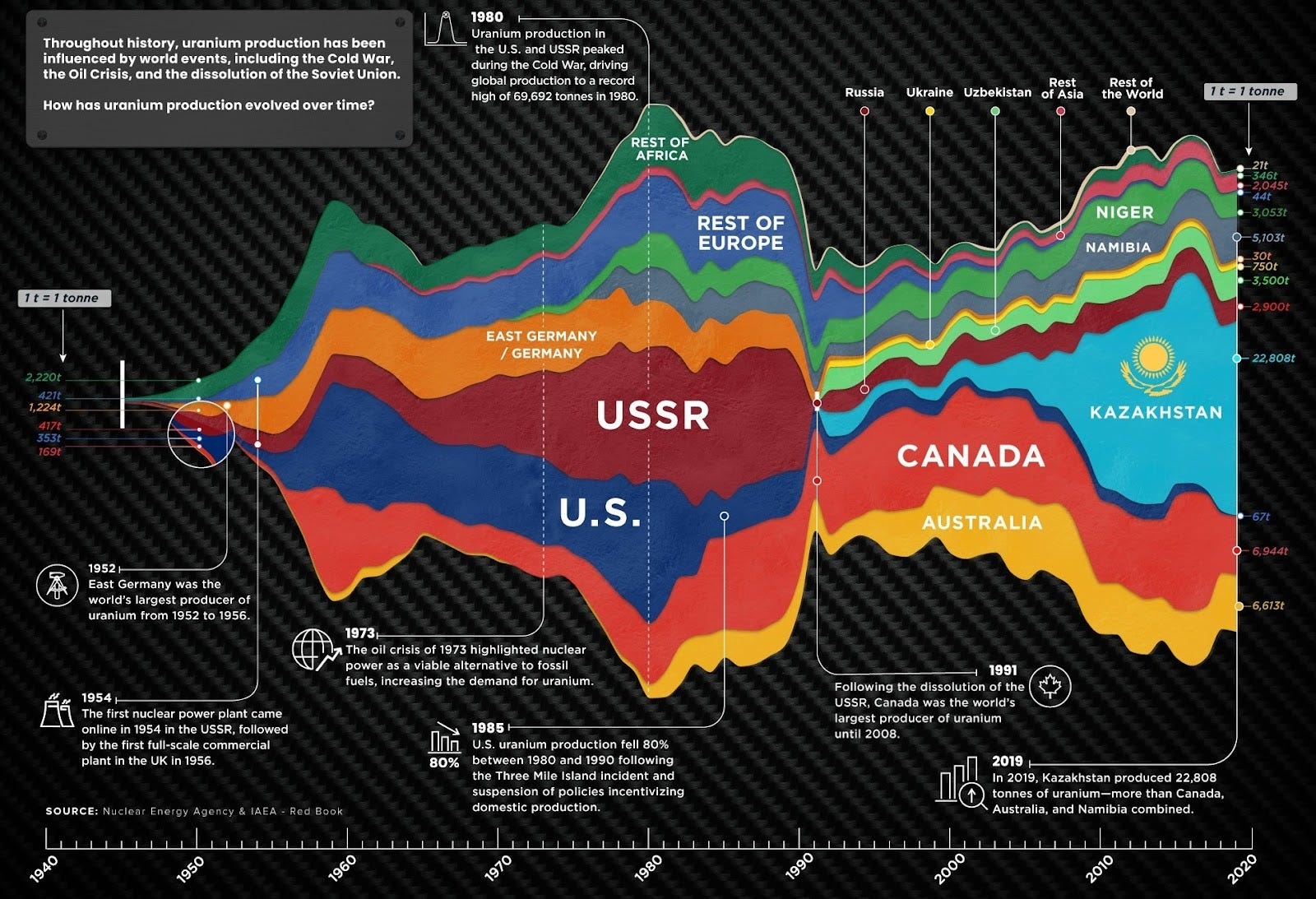

XI. Kazakhstan and Russia: The Uncomfortable Reality of Concentration

Any serious discussion of uranium must confront an awkward fact:

roughly 40% of global uranium production comes from Kazakhstan.

That dominance was built on low-cost in-situ leaching, scale, and decades of investment. But it also introduces fragility:

- production is concentrated,

- supply chains depend on chemicals like sulphuric acid,

- and long-term output is expected to decline as existing mines mature.

At the same time, enrichment capacity remains heavily skewed toward Russia.

This creates a structural asymmetry:

- the West consumes uranium,

- but critical steps in the fuel cycle are externally exposed.

India understands this vulnerability acutely because it lived through decades of nuclear isolation. That experience explains its reluctance to rely on any single supplier — even friendly ones.

It also explains why fuel-cycle control remains central to India’s long-term thinking.

XII. The Thorium Question Returns — But This Time, It’s Real

For decades, thorium occupied an awkward place in nuclear discourse:

celebrated in theory, elusive in practice.

That changed when China confirmed successful thorium-to-uranium-233 breeding inside an operating molten-salt reactor.

This achievement matters for three reasons.

First, it validates a concept that had remained largely experimental for over half a century. Thorium is not fissile, but when it absorbs a neutron, it can be converted into uranium-233, a usable reactor fuel. China has now demonstrated that conversion inside a functioning reactor, not a lab.

Second, molten-salt reactors change nuclear architecture itself. Unlike traditional reactors that rely on solid fuel rods and high-pressure water systems, molten-salt designs dissolve fuel into liquid salts that:

- operate at atmospheric pressure,

- enable passive safety,

- allow continuous refuelling,

- and dramatically reduce meltdown risk.

Third, this breakthrough reshapes long-term fuel economics. Thorium is far more abundant than uranium, and its utilisation could eventually ease uranium scarcity.

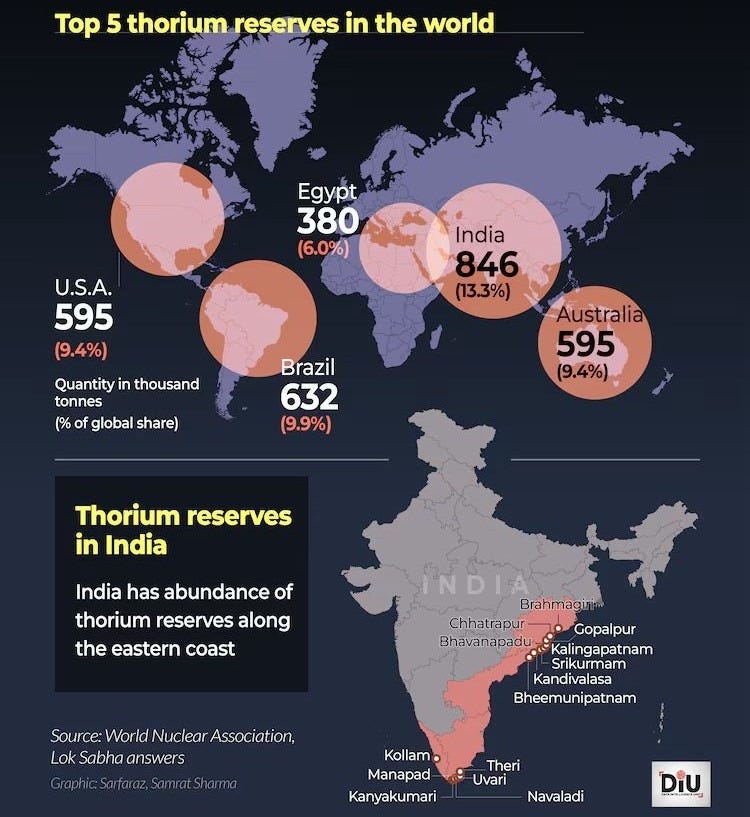

For India, this development is especially consequential.

India possesses one of the world’s largest thorium reserves. Homi Bhabha’s three-stage programme was built around precisely this logic. What China has done is compress a seventy-year aspiration into an operational data point.

This does not mean thorium reactors are commercially ready. Scaling molten-salt technology remains difficult:

- materials corrosion,

- regulatory unfamiliarity,

- fuel handling complexity,

- and capital risk all remain unresolved.

But the strategic horizon has shifted.

Thorium is no longer speculative.

It is proven in operation.

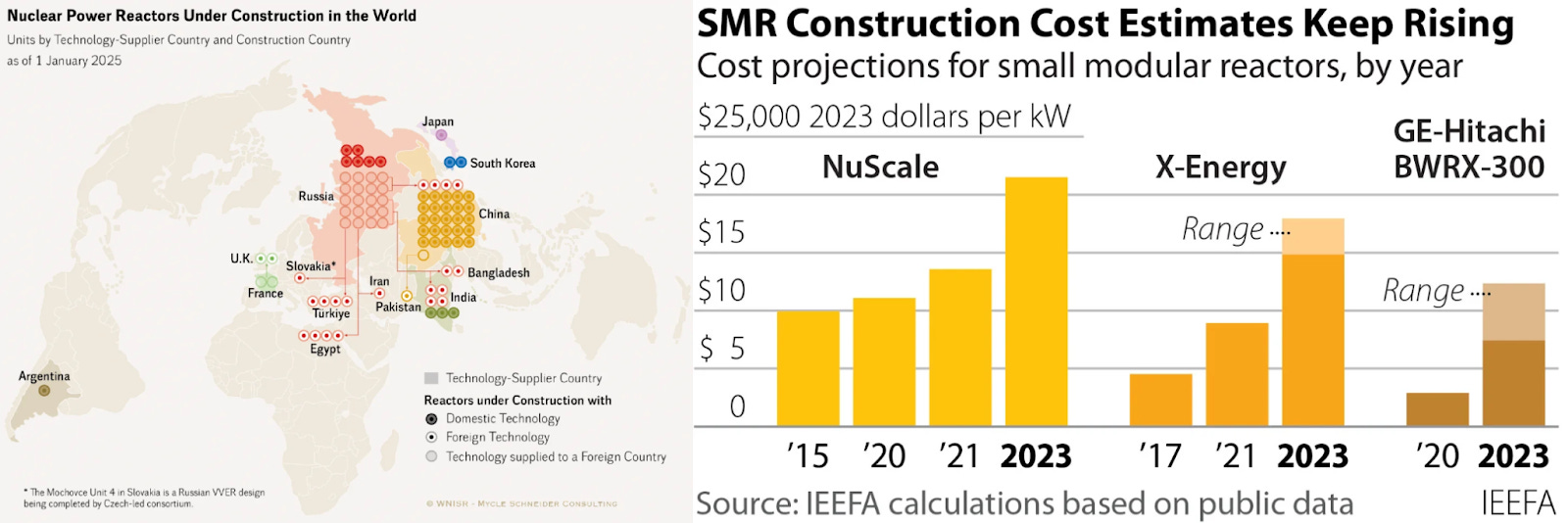

XIII. Small Modular Reactors: Speed, Not Size, Is the Breakthrough

Large nuclear plants will continue to matter for grid-scale power. But the most important nuclear innovation of the 2020s is not size — it is modularity.

Small Modular Reactors (SMRs) aim to solve nuclear’s historic weaknesses:

- decade-long construction timelines,

- massive upfront capital,

- site-specific engineering risk.

By standardising designs and manufacturing components in factories, SMRs promise:

- faster deployment,

- lower initial capital exposure,

- greater siting flexibility,

- and better integration with industrial users.

India’s approach to SMRs reflects hard-earned realism.

Rather than leap directly to exotic designs, India’s Bharat Small Modular Reactor is based on proven pressurised water technology, using slightly enriched uranium and layered passive safety systems. The goal is not technological heroics, but predictable execution.

SMRs also align with India’s emerging electricity demand profile:

- repurposing retiring coal plants,

- supplying captive power to heavy industry,

- powering data centres,

- and serving remote or off-grid regions.

In this sense, SMRs are less about revolution and more about deployment velocity.

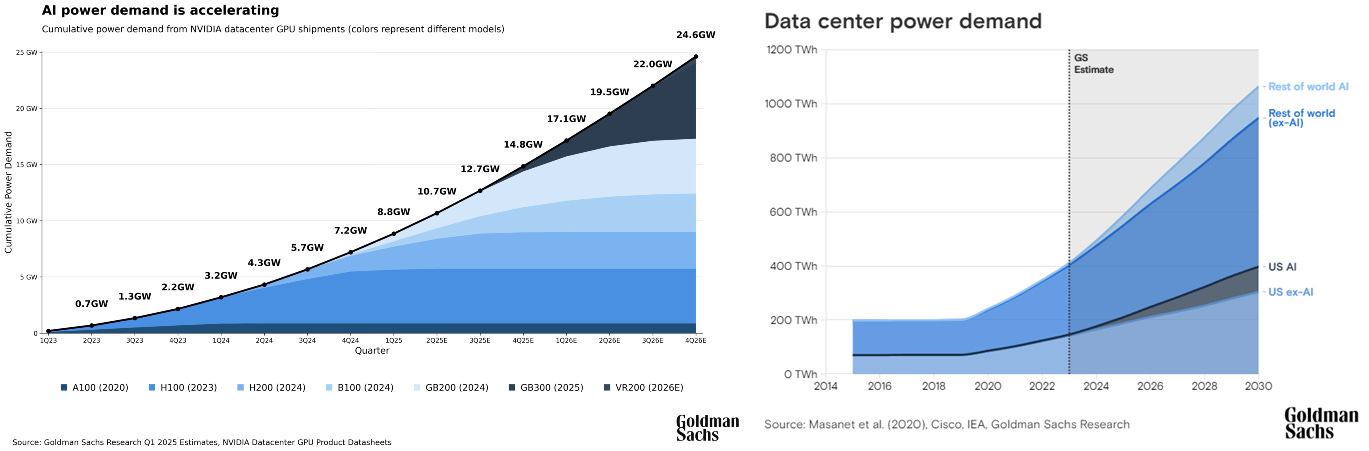

XIV. AI and Data Centres: The Forcing Function No One Planned For

Every energy transition has a forcing function – an external pressure that collapses debate into action.

For nuclear’s return, that force is computation.

AI workloads are energy-intensive, continuous, and intolerant of interruption. Training and inference cannot pause for cloud cover or weak winds. This is why hyperscalers are no longer talking about “green power” in abstract terms. They are locking in baseload electricity for decades.

Solar and wind can contribute, but they cannot guarantee 24×7 availability without massive overbuild and storage that remains economically fragile.

Nuclear can.

This is why:

- mothballed reactors are being revived,

- utilities are signing 20-year power purchase agreements,

- and tech firms are directly funding nuclear capacity.

For India, the implication is profound.

India is positioning itself as a global data-centre hub, offering tax incentives to foreign cloud providers. But data centres do not run on intent. They run on stable electricity.

SMRs and nuclear expansion are therefore not peripheral to India’s digital ambitions. They are foundational.

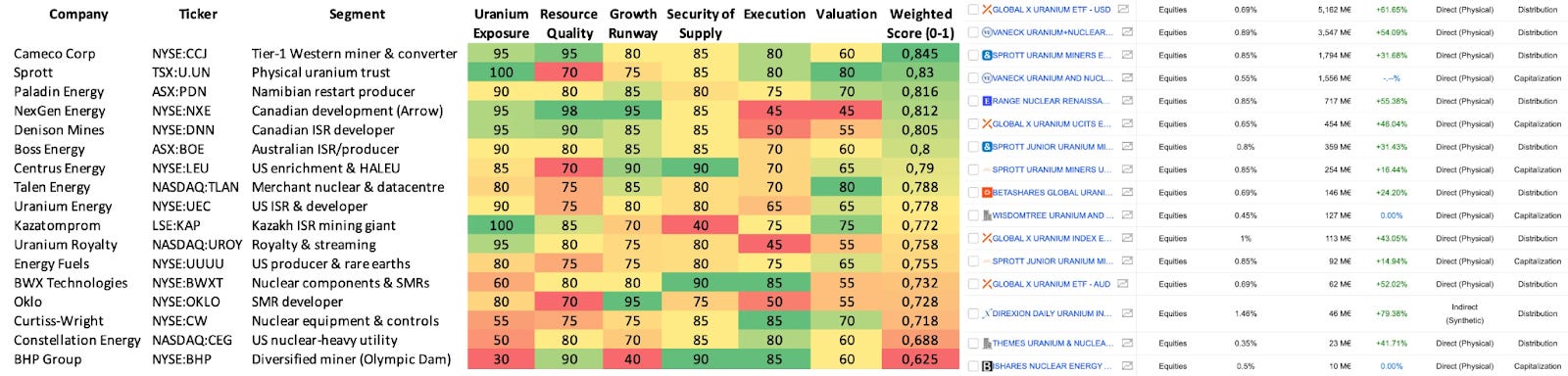

XV. Capital Markets Are Not Guessing. They Are Mapping Constraints

When narratives change, markets speculate.

When constraints harden, markets reallocate.

The structure of nuclear-focused ETFs reveals how capital is interpreting the transition:

- fuel-heavy ETFs overweight uranium producers, reflecting belief in long-term scarcity;

- miner-focused funds amplify exposure to undeveloped assets, signalling confidence that new supply will be needed;

- balanced funds include utilities and component manufacturers, pricing in reactor life-extensions and build-outs.

What is striking is not disagreement, but convergence.

Across diversified funds, high-conviction miners, junior explorers, and system-level ETFs, the same choke points appear repeatedly:

- uranium supply,

- enrichment capacity,

- reactor construction expertise,

- and licensed operating assets.

This mirrors government behaviour almost exactly.

States are securing fuel.

Utilities are locking contracts.

Capital is positioning around the same constraints.

That alignment is rare.

XVI. India’s Endgame: Time, Sovereignty, and Optionality

Viewed together, India’s recent moves form a coherent strategy.

In the short term:

- secure uranium from trusted partners,

- liberalise mining and processing,

- extend reactor lifetimes,

- deploy SMRs where speed matters.

In the medium term:

- deepen private sector participation,

- integrate into global nuclear supply chains,

- and stabilise grids for industrial growth.

In the long term:

- preserve fuel-cycle autonomy,

- keep thorium pathways alive,

- and avoid technological dependence on any single power bloc.

India is not betting on a single future.

It is buying optionality.

That is the defining feature of serious energy strategy.

XVII. The Deeper Truth of the Energy Transition

The energy transition was never about replacing one technology with another.

It was about answering harder questions:

- Who controls fuel?

- Who controls materials?

- Who controls time?

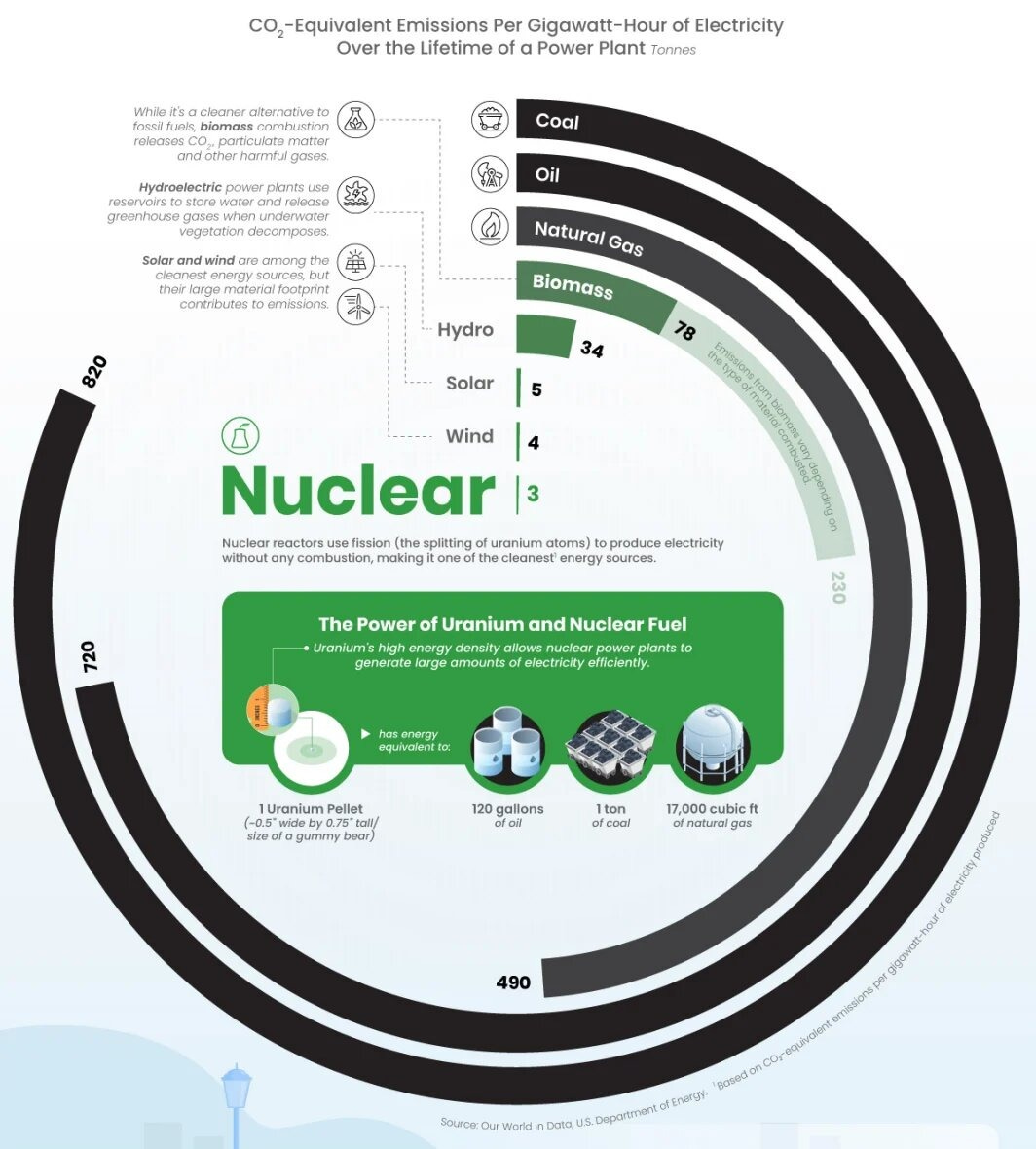

Solar and wind answer emissions.

Nuclear answers continuity.

As electrification accelerates, grids become less forgiving. As materials tighten, supply chains become strategic. As computation scales, power becomes non-negotiable.

Nuclear does not solve every problem.

But without it, the transition accumulates fragility faster than resilience.

XVIII. Conclusion: This Is No Longer a Debate

The most important shift is not technological or political.

It is temporal.

The question is no longer whether nuclear belongs in the energy transition.

That question has already been answered – by physics, by grids, by policy, and by capital.

The real question now is:

Who moves fast enough before fuel, materials, and execution capacity become binding constraints?

India’s recent actions suggest it understands this clearly.

The rest of the world is catching up.

Disclaimer: I am not a registered SEBI Research Analyst and anything in the above article should not be construed as a recommendation. This should be read solely for education purposes.