How Nuclear, Materials, and Fuel Cycles Are Quietly Rewriting the Global Power Order

This is a 2-part series on how Nuclear energy is the future and how India might become a global powerhouse in next 2 decades, if things go as per plans.

The 2nd part will be released on Saturday morning. Make sure to read that too.

I. The Story We’ve Been Telling Ourselves (And Why It’s Incomplete)

For more than a decade, the global energy transition has been sold as a clean substitution problem.

Coal out. Solar and wind in. Add batteries. Electrify everything. Problem solved.

This story is comforting because it frames decarbonisation as a linear engineering challenge rather than a systemic one. Replace dirty inputs with clean ones, scale fast enough, and emissions fall. And for a while, the numbers seemed to cooperate. Solar costs collapsed. Wind farms spread across continents. Installed renewable capacity surged.

But beneath the charts and press releases, the energy system was accumulating structural stress.

Not ideological stress.

Not political stress.

But, Physical stress.

Electricity grids do not operate on narratives. They operate on frequency, inertia, reliability, materials, fuel logistics, and long-duration availability. And as renewable penetration increased, a deeper contradiction began to surface – one that markets, policymakers, and now even retail investors are being forced to confront.

The transition was never just about clean generation.

It was always about reliable power at scale.

And that distinction changes everything.

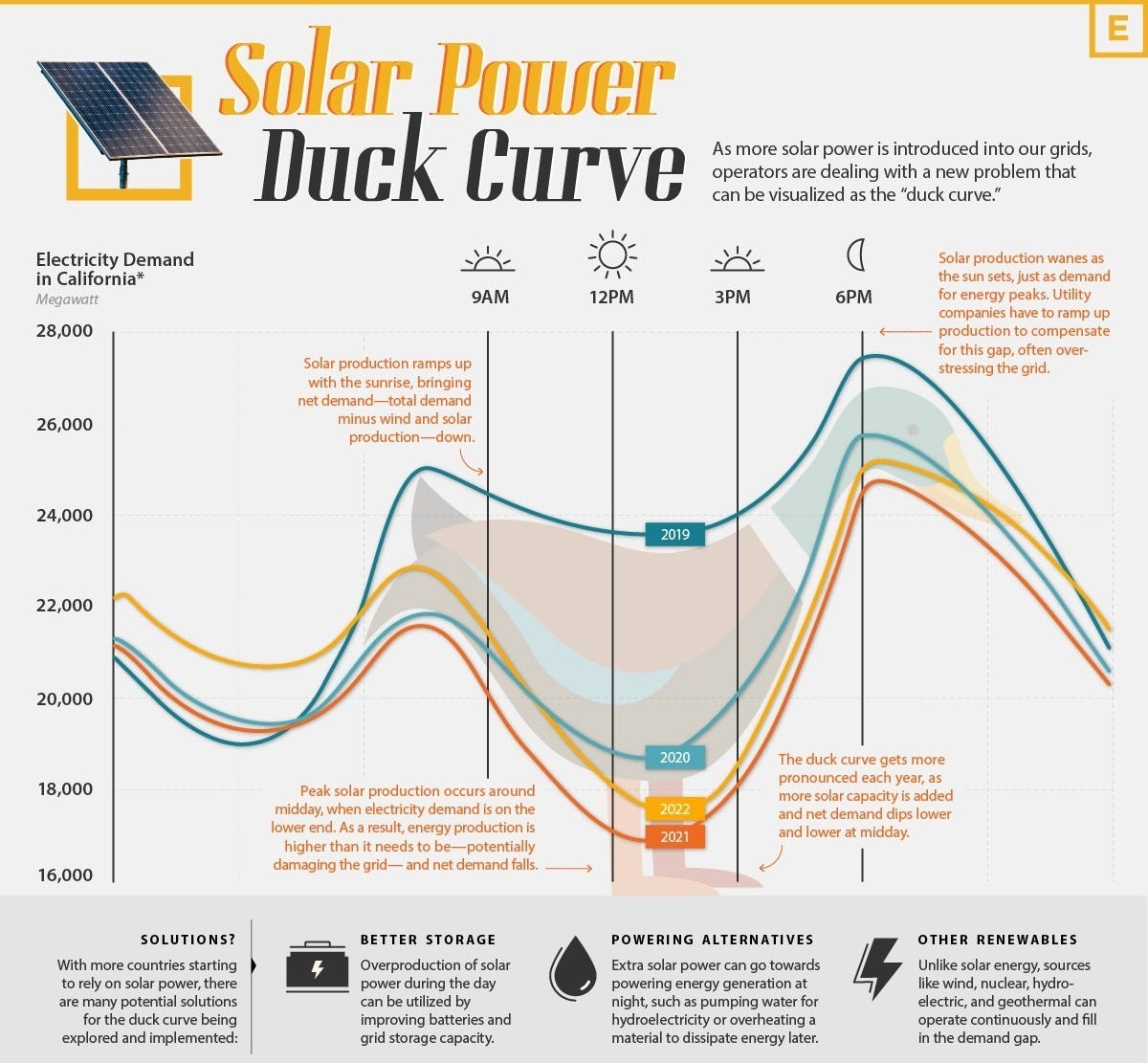

II. Solar’s Hidden Constraint: Time, Not Emissions

Solar energy’s greatest strength is its simplicity, but is also its greatest limitation.

Once installed, photovoltaic panels generate electricity with near-zero operational emissions. But solar output is governed by a variable no grid operator controls: the Sun.

Generation peaks at midday.

Demand peaks after sunset.

This temporal mismatch isn’t a rounding error. It is a structural flaw that grows worse, not better, as solar penetration increases.

To compensate, grids require:

- massive transmission expansion,

- short-duration storage,

- and dispatchable backup power.

Each layer adds cost, complexity, and degradation risk. Batteries, while improving, remain economically viable only for hours, not days or weeks. Seasonal storage remains unsolved at scale.

The result is a paradox:

Countries with the fastest solar growth still rely heavily on fossil fuels—or must accept growing grid fragility.

This is not an argument against solar.

It is an argument against solar absolutism.

At industrial scale, a modern grid needs at least one source of power that is:

- predictable,

- dispatchable,

- scalable,

- and low-carbon.

Only one technology consistently meets all four.

Nuclear.

III. Nuclear’s Return Is Not Ideological—It’s Mathematical

Nuclear power never failed because it didn’t work.

It failed because:

- capital costs were front-loaded,

- construction timelines were long,

- public trust eroded after rare but catastrophic accidents,

- and cheap fossil fuels delayed hard decisions.

But none of those factors changed nuclear’s physics.

A nuclear reactor produces power:

- continuously,

- independent of weather,

- with negligible carbon emissions,

- and at energy densities orders of magnitude higher than any chemical fuel.

As electricity demand accelerates – driven by electrification, industrial reshoring, data centres, and AI – the shortcomings of intermittent systems become unavoidable.

This is why nuclear keeps re-entering policy discussions regardless of political ideology.

And it’s why countries as different as India, China, the United States, Russia, and France are converging on the same conclusion at roughly the same time.

Not because they agree with each other.

But because the grid does not negotiate.

IV. The Material Reality of “Clean” Energy

Here’s where the transition narrative becomes uncomfortable.

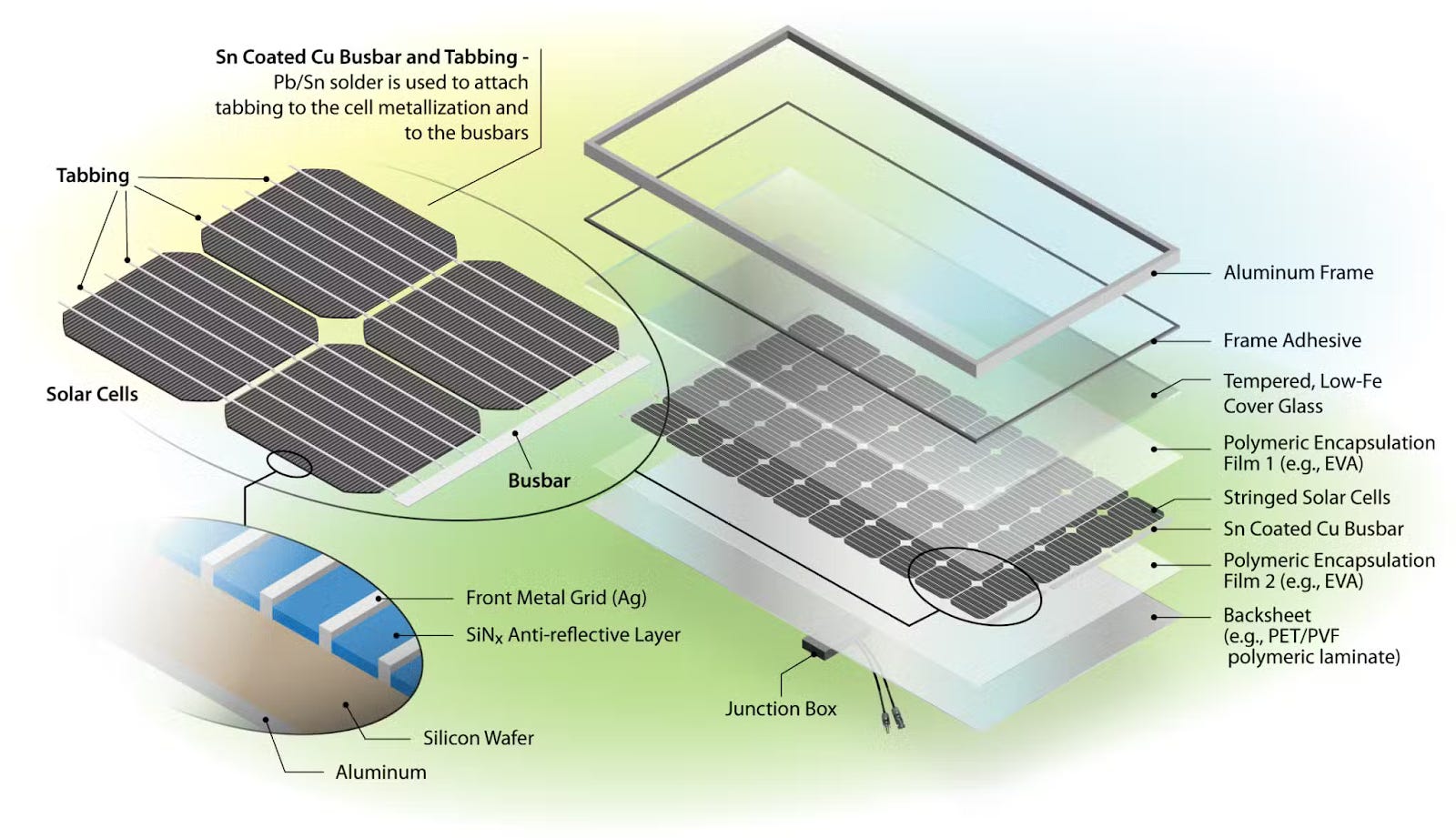

Solar panels do not burn fuel, but they consume materials. A lot of them.

Silicon for cells.

Aluminium for frames.

Copper for wiring, inverters, transformers, and grids.

Silver for electrical contacts.

High-purity glass for protection.

Per unit of reliable electricity capacity, solar is far more material-intensive than coal, gas, or nuclear. And every one of those materials must be mined, processed, transported, and refined, mostly using fossil fuels.

This creates a second-order effect the energy debate long ignored:

Decarbonisation shifts the bottleneck from emissions to extraction.

Mining damage is local and immediate.

Benefits of clean electricity are distant and diffuse.

As renewable deployment scales globally, demand for copper and aluminium doesn’t just rise. It explodes. And supply is not keeping pace.

India’s own policy documents project copper demand rising to nearly 10 million tonnes by 2047, while acknowledging that over 90% of copper concentrate may need to be imported. Domestic reserves exist, but only a fraction are economically accessible.

This is why India is:

- courting foreign miners,

- offering incentives for smelters and refineries,

- embedding copper clauses into free-trade agreements,

- and sending geologists abroad to secure overseas assets.

Copper is not optional.

It is the circulatory system of electrification.

And nuclear power, while materially lighter per unit of energy, introduces its own constraint.

Fuel.

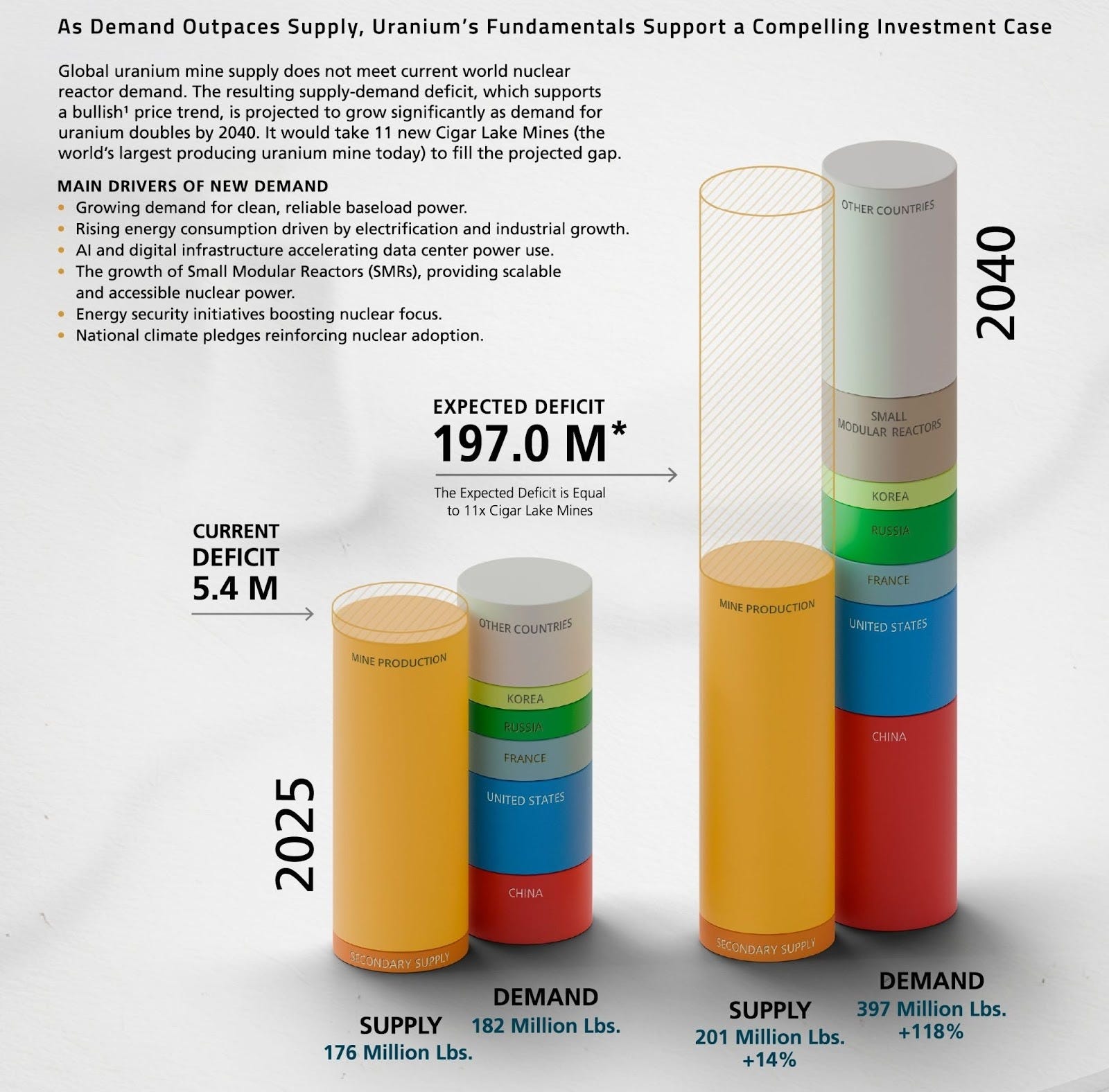

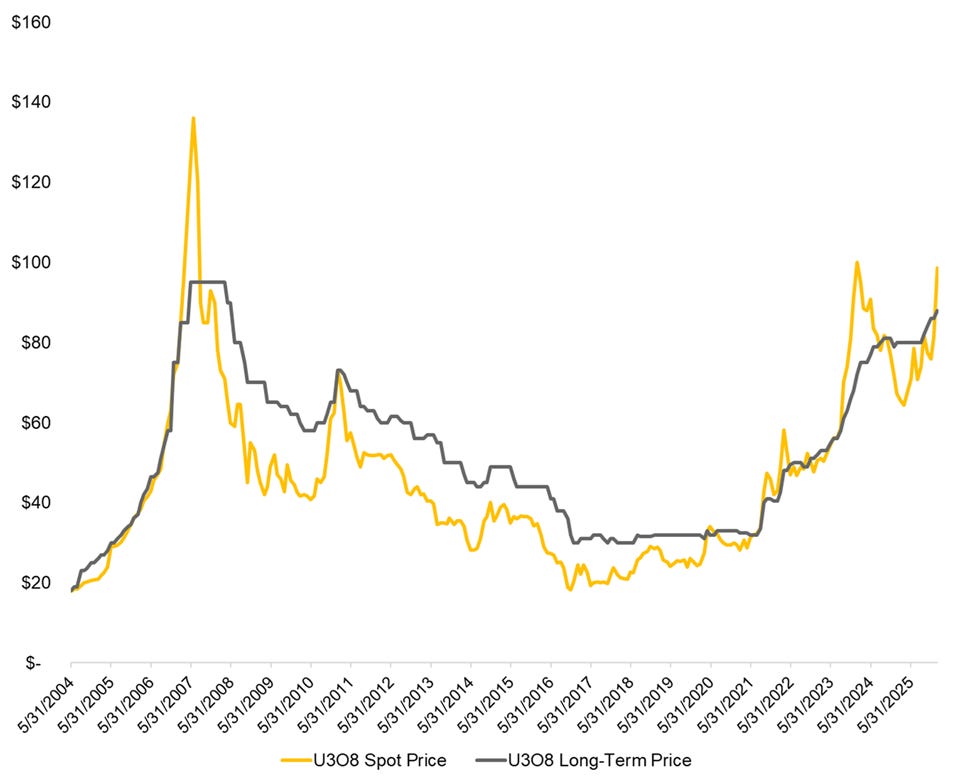

V. Uranium: The Quiet Bottleneck No One Can Ignore

Uranium is not oil.

You cannot buy it freely on spot markets during shortages.

You cannot rapidly ramp production when prices spike.

You cannot ignore geopolitics.

The uranium market is:

- regulated,

- contract-driven,

- capital-intensive,

- and slow to respond.

Global reactor demand already exceeds mined supply. The gap has been filled using secondary sources—stockpiles, re-enrichment, and inventory drawdowns. These buffers are finite.

At the same time:

- China is building reactors faster than any country in history.

- Russia continues exporting nuclear plants bundled with fuel contracts.

- Europe is extending reactor lifetimes.

- India plans to expand nuclear capacity more than twelve-fold by 2047.

Analysts estimate that India alone could add uranium demand equivalent to 30% of today’s global production.

This is why uranium prices have rebounded sharply.

This is why long-term contracts are replacing spot purchases.

This is why fuel security has become a diplomatic issue.

And this is why capital markets are no longer treating uranium as a forgotten commodity.

VI. India’s Nuclear Trajectory: A Long Bet Re-Awakening

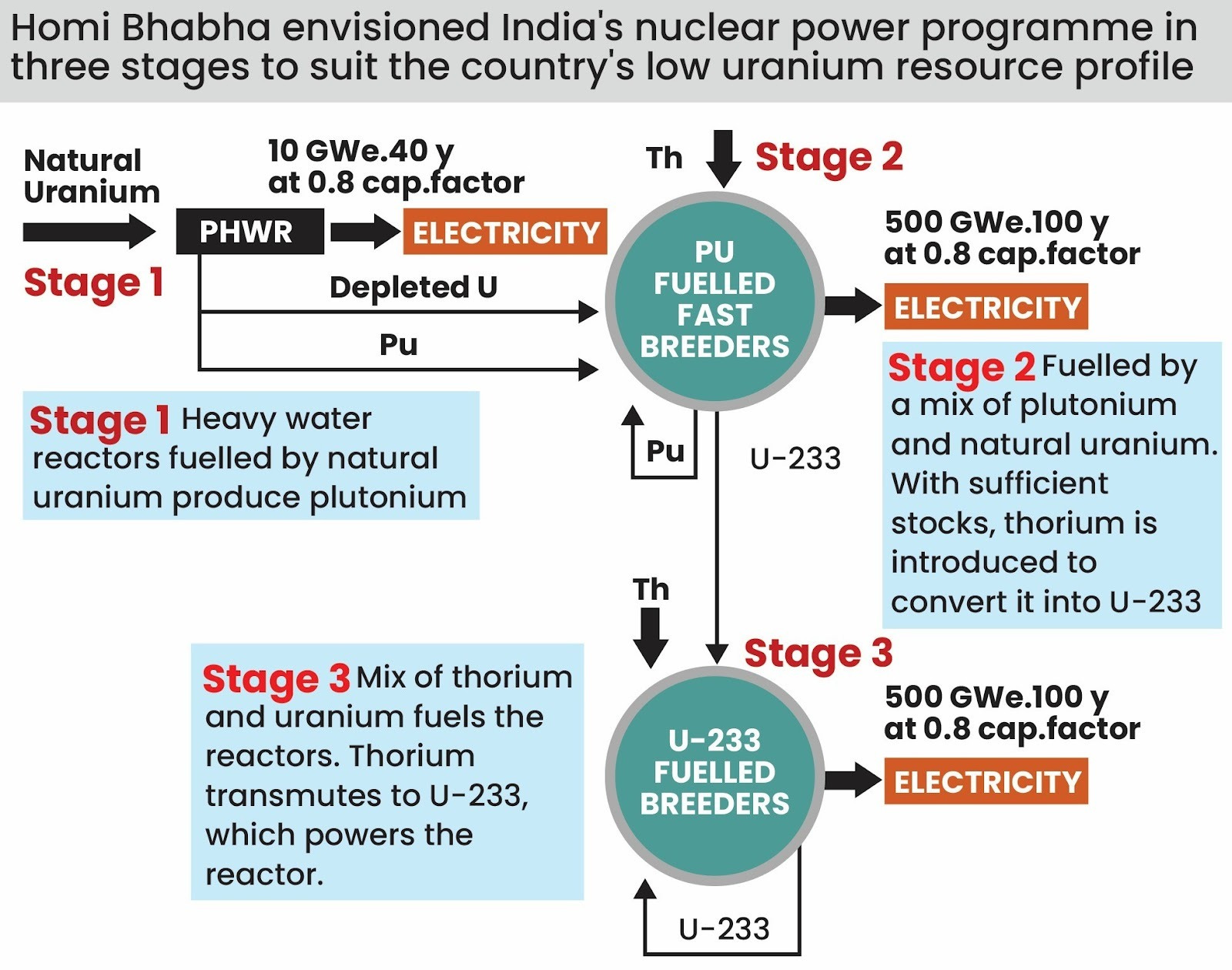

India’s nuclear story is often misunderstood as delayed or unsuccessful. In reality, it is unfinished.

In the 1950s, Dr. Homi Bhabha articulated a three-stage programme aimed at energy independence through thorium – an element India possesses in abundance but cannot use directly as fuel.

The plan required:

- heavy water reactors to produce plutonium,

- fast breeder reactors to convert thorium into uranium-233,

- and finally, thorium-based reactors.

Technically sound. Strategically elegant.

But execution was slow.

Leadership disruptions, decades of trade embargoes, exclusion from global nuclear commerce, and rigid state monopolies all compounded delays. India remained outside the Nuclear Non-Proliferation Treaty and was largely cut off from uranium markets for over three decades.

That isolation shaped India’s nuclear DNA:

self-reliance, caution, and fuel-cycle ambition.

Today, that long-term vision is colliding with short-term reality.

India needs reliable power now.

It needs uranium now.

And it needs scale faster than state-only execution can deliver.

VII. Policy Inflection: Why Everything Is Changing Now

Over the last two years, India has quietly rewritten its nuclear playbook.

- Liability laws are being aligned with international norms.

- Private sector participation is being opened.

- Small Modular Reactors (SMRs) are receiving dedicated funding.

- Customs duties on nuclear equipment are being waived until 2035.

- Uranium mining and processing monopolies are being dismantled.

- Long-term fuel contracts are being secured abroad.

These are not isolated reforms.

They are sequenced.

Fuel first.

Then technology.

Then capital.

The objective is not ideological liberalisation.

It is execution under constraint.

India is preparing for a world where:

- uranium is scarce,

- electricity demand is relentless,

- grids cannot tolerate intermittency alone,

- and geopolitical shocks are the norm, not the exception.

VIII. Why This Matters Beyond India

What’s happening in India is not unique.

It is representative.

Across the world, governments are rediscovering a truth they once avoided:

Energy transitions are not just about cleaner inputs—they are about control over systems.

Who controls fuel.

Who controls materials.

Who controls construction capacity.

Who controls long-duration power.

Nuclear power forces these questions into the open because it exposes every weakness in supply chains, institutions, and planning horizons.

And this is why nuclear’s return is being priced not just by states—but by markets.

Once control becomes the lens, the transition stops looking like a race toward renewables and starts looking like a contest over bottlenecks. Uranium supply that cannot be scaled on demand. Enrichment capacity concentrated in a handful of jurisdictions. Reactor construction capability that takes decades to rebuild once lost. And materials like copper that quietly dictate how fast electrification can proceed at all. These are not theoretical risks — they are active constraints that harden as deployment accelerates.

Stepped back, the pattern is hard to miss. The energy transition is no longer constrained by ambition or technology, but by materials, fuel cycles, and system-level reliability. These are slow-moving variables, resistant to slogans and immune to deadlines. Once they assert themselves, policy flexibility narrows quickly. And this is precisely the phase the transition has now entered.

If you’ve read this far, your attention span has already outperformed most long-term energy forecasts.

On Saturday, we trace these constraints to their logical endpoint – uranium geopolitics, advanced reactors, and the quiet alignment of state strategy and capital.