For the first time in a generation, Gold is no longer just a “hedge”. It has become a global obsession. As we move through 2026, the yellow metal has shattered every psychological barrier, with domestic prices in India testing the ₹1.4 lakh mark and international spot prices eyeing the $5,000 mountain. To the casual observer, the trajectory looks like a one-way street.

But for the disciplined investor, the most dangerous time is when a narrative becomes “unanimous.” While the structural case for gold remains robust, a unique cluster of counter-forces is quietly assembling. From the “Trump Tariff” trap to the mechanics of “Resource Nationalism,” the road to $5,000 is likely to be paved with a brutal correction that will catch the “FOMO” crowd off guard.

The “Trump Tariff” Trap: Inflation vs. Growth

The prevailing thesis among many investors is something like this: President Trump’s aggressive tariff regime will drive up the cost of imports, reigniting inflation in US. Higher inflation will lead to higher interest rates by Fed, which would divert money to US treasuries, as ”Real Yield” will be higher there. However, this logic ignores the Fed’s Dilemma.

If tariffs act as a “tax on the consumer,” they don’t just raise prices. They kill growth. We are currently witnessing a tug-of-war between two outcomes:

- The Reflationary Spike: If the economy stays strong despite tariffs, the Fed will be forced to keep interest rates “higher for longer” to fight rising prices. This pushes Real Yields (Interest minus Inflation) higher. When you can get a guaranteed 6% return on a US Treasury, the 0%-yielding Gold suddenly looks expensive.Source: www.longtermtrends.com

- The Growth Shock: Conversely, if tariffs trigger a global recession, the Fed might be forced to cut rates to save the economy, even if inflation is high. This “Stagflation” scenario is the rocket fuel for Gold.

The danger for Gold investors today is that the market has already priced in the “Stagflation” win. Any sign that the US economy is absorbing tariffs better than expected could trigger a massive “Liquidity Flush” in precious metals.

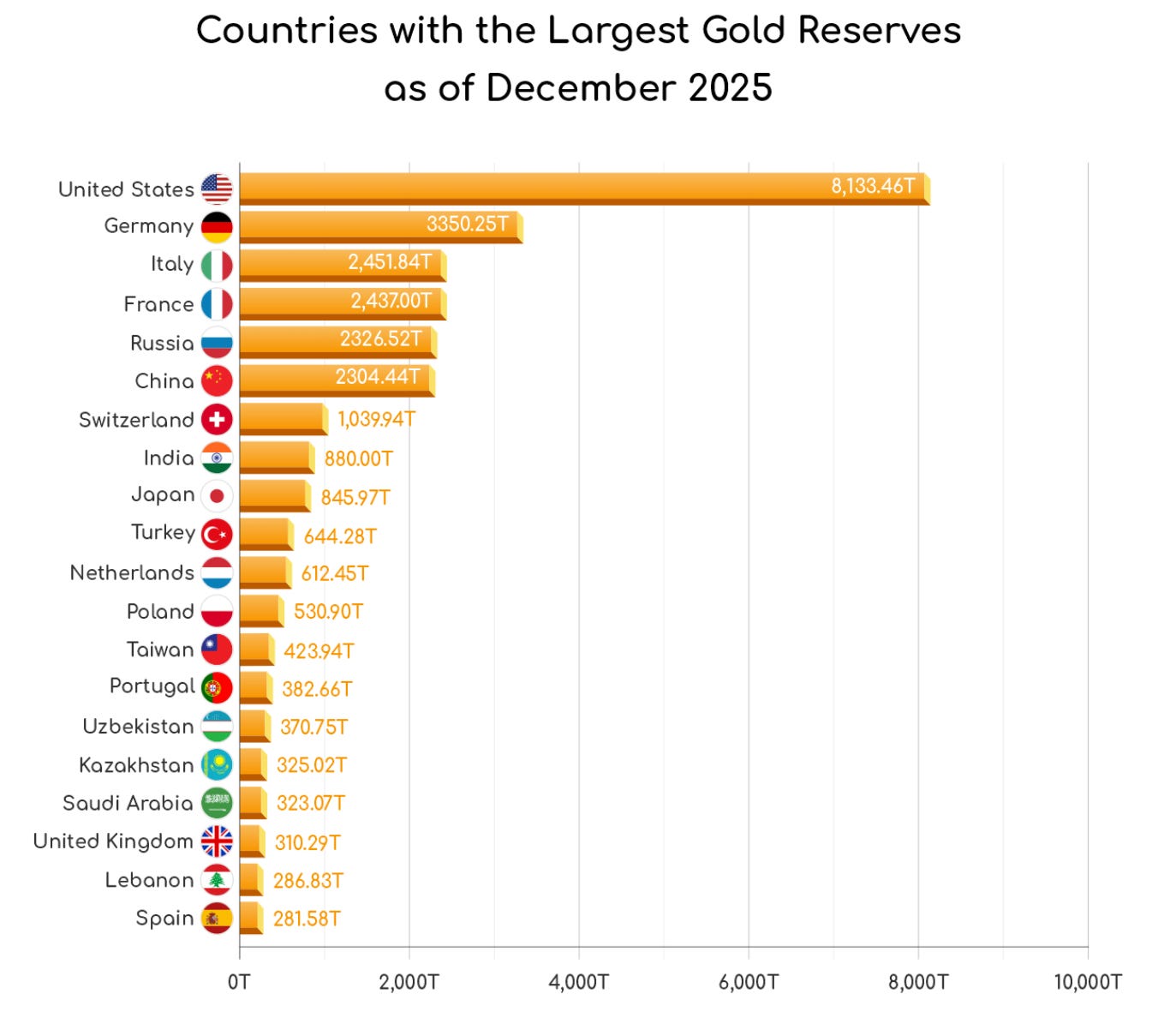

The Silent Exit: Central Banks and “Buying Pauses”

The “floor” of the current gold market has been built by Central Banks, specifically the PBoC (China) and the RBI (India). Driven by a desire to diversify away from a “weaponized” US Dollar, these institutions have been the “Whales” of the market.

However, Central Banks are not “dumb money.” They are price-sensitive. In mid-2025, we saw the first cracks when the PBoC paused its gold accumulation for several months simply because prices had run too far, too fast. If the world’s biggest buyers decide that $4,600 is “overvalued,” the psychological support for retail investors will vanish. When the Whale stops swimming, the smaller fish get stranded.

Source: World Gold Council, IMF International Financial Statistics

The Sprott Effect and the Liquidity Paradox

In the US, the rise of “Physical Trusts” like Sprott has changed how Gold is held. Unlike traditional “Paper ETFs,” these trusts hold massive physical reserves in global hubs like Singapore and Rotterdam.

This has created a Liquidity Paradox. Because so much physical gold is now locked in these private trusts, the “Float” (available gold for trading) has shrunk. While this pushes prices up during a boom, it creates a “Trap Door” effect during a sell-off. If a major hedge fund needs to raise cash to cover losses in a volatile tech market, they will dump their most profitable asset: Gold. In a thin market, a small sell order can trigger a “Flash Crash.”

Resource Nationalism: The New Wildcard

We are moving into an era of Resource Nationalism. Countries are no longer just trading commodities; they are hoarding them as strategic infrastructure. While this sounds bullish for Gold, it introduces a “Supply Shock” risk.

If major gold-producing nations, facing their own currency crises, decide to liquidate a portion of their “Strategic Reserves” to stabilize their domestic economies, the market could see a sudden, unexpected influx of physical bars. In a world of fracturing alliances, Gold is the only “neutral” currency, but that also makes it the first asset a desperate government will sell to stay afloat (similar to how RBI sells USD to avoid depreciation, they can start offloading Gold whenever required).

The “Common Man” Strike

Finally, we must look at the grassroots level. In India and China (the biggest markets for Gold for common man), gold is not just an asset; it is a cultural cornerstone. But at ₹1.4 lakh per 10 grams, we are reaching the point of demand destruction. Jewelry hubs in Mumbai and Shanghai are reporting record-low footfalls. For the first time, households are becoming “Net Sellers,” recycling old family gold to lock in profits rather than buying new sets for weddings. When the world’s two largest physical consumers go on a “Buyer’s Strike,” the market becomes entirely dependent on speculative Wall Street money. And as we know, speculative money is the first to leave the room when the lights flicker.

Investment Thesis: Time vs. Price

Does this mean the Gold story is over? Absolutely not. As long as global debt continues to climb and the “Reserve Currency” status of the USD is questioned, Gold remains an essential part of the portfolio.

However, the “Buy at any price” phase is over. We will likely enter a Time Correction soon, a period where Gold might trade sideways or correct by 15-20% to digest its recent gains for some weeks or months.

My approach? Stop chasing the “Green Candles.”

- I am avoiding lump-sum investments at these psychological peaks.

- And utilizing a Systematic Investment Plan (SIP) to average out costs over the next 12 months.

- Putting Gold to be 15% of my total portfolio.

- Watching the Real Yields and PBoC announcements more than the headlines.

In a market fueled by “Uncle Trump’s” tweets and Central Bank secrecy, the most valuable asset you own isn’t the Gold in your locker. It’s the discipline to wait for the right entry.

Disclaimer: I am not a registered SEBI Research Analyst and anything in the above article should not be construed as a recommendation. This should be read solely for education purposes.