How to position your portfolio amidst the rising divergence?

When we think about markets, our first instinct is usually to look at the stock market. After all, equities dominate headlines and capture investor imagination. But in truth, the bond market is the backbone of the financial system, and bond yields often dictate the direction of everything else—from the cost of bank loans to the profitability of corporations, to even stock market valuations.

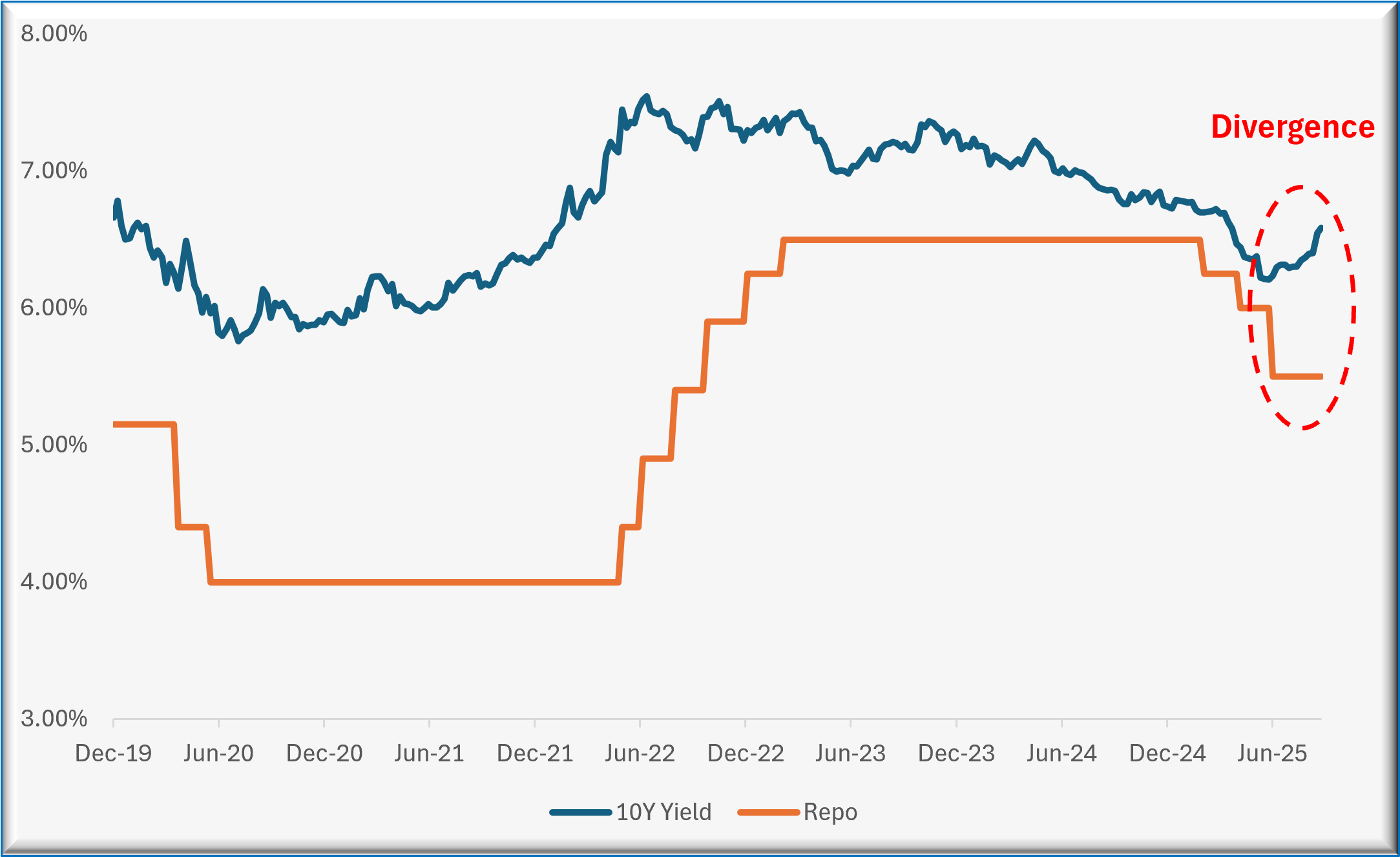

In India today, the bond market is flashing signals that investors cannot ignore. While the RBI has been cutting rates aggressively and injecting liquidity, government bond yields are rising—a divergence that carries profound implications for the economy, financial institutions, and investors.

The Inverse Dance: Understanding Bond Dynamics

At the core, bond prices and yields move in opposite directions. When bond prices rise, yields fall, and vice versa. The yield represents the return earned by holding a bond until maturity—essentially the market’s assessment of what compensation is required for lending money to the government.

Typically, bond yields track the repo rate—the rate at which the RBI lends to commercial banks. When the central bank cuts rates, borrowing costs should decline across the economy, pulling bond yields lower.

But 2025 has shattered this conventional wisdom.

The Great Divergence: Numbers That Tell a Story

The Reserve Bank of India has delivered an aggressive 100 basis points of rate cuts in 2025, bringing the repo rate down from 6.50% to 5.50%. The cuts came in measured doses—25 basis points each in February and April, followed by a decisive 50 basis point reduction in June as growth concerns mounted.

Simultaneously, India achieved a milestone that should have celebrated in bond markets: S&P Global Ratings upgraded India’s sovereign credit rating to ‘BBB’ from ‘BBB-‘ in August 2025, marking the country’s first rating upgrade in 18 years. This vote of confidence typically translates to lower borrowing costs as global investors view the country as a safer bet.

Adding to the positive narrative, the government announced sweeping GST reforms under the ‘GST 2.0’ framework, simplifying the current complex four-tier structure (5%, 12%, 18%, 28%) into a streamlined two-tier system of 5% and 18%. Most goods currently taxed at 12% will move to the 5% bracket, while approximately 90% of items in the 28% category will shift to 18%. This represents a substantial tax cut designed to boost consumption and revive economic momentum.

Yet despite this trifecta of positive developments, the 10-year government bond yield has climbed to 6.65% last week (closed at 6.59% latest), up from 6.13% in June. The spread between the benchmark 10-year yield and the repo rate has widened to levels not seen since Jan 2023.

The message from bond traders is clear: the risks outweigh the positives.

Decoding the Market’s Concerns

Fiscal Arithmetic Under Pressure

The GST rate cuts, while politically popular and economically stimulative, create an immediate challenge: a significant reduction in government revenue. When goods migrate from higher to lower tax brackets, the fiscal math becomes strained.

The government must bridge this revenue gap somehow, and the most likely source is increased borrowing through additional bond issuances. Basic economics dictates that when bond supply increases without proportional demand growth, prices fall and yields rise.

Market participants are scrutinizing whether the government can maintain its fiscal deficit target of 4.4% of GDP for FY2025-26 in light of these revenue pressures. Any slippage could trigger further bond market stress.

External Shocks: The Trump Tariff Reality

India faces an unprecedented external challenge with President Trump’s 50% tariffs on Indian goods, which took effect on August 27, 2025. These tariffs target India’s purchases of Russian oil and broader trade practices, potentially slashing India’s exports to the US from $87 billion to around $50 billion by 2026.

This trade shock creates multiple pressure points:

- Reduced export revenues weakening the current account

- Potential need for government support to affected industries

- Currency pressure requiring intervention

- Overall economic growth deceleration

The bond market is pricing in the fiscal cost of managing these external headwinds.

The Supply-Demand Catastrophe

Perhaps most tellingly, despite the RBI’s extraordinary liquidity injection of ₹3.05 lakh crore through Open Market Operations between March and May 2025, bond yields have refused to decline sustainably. This suggests that selling pressure and new bond supply are overwhelming even aggressive central bank intervention.

The mathematics are stark: gross long-bond supply is estimated at ₹11.98 trillion, significantly exceeding the anticipated demand from traditional buyers like insurance companies, pension funds, mutual funds and provident funds.

Foreign Capital Flight

The retreat of foreign investors adds another layer of complexity. Foreign Institutional Investors have withdrawn $9.2 billion from Indian equities in 2025, while debt market outflows surged to $2.27 billion in April—the largest monthly exodus since May 2020.

The narrowing of the India-US 10-year yield spread to approximately 200 basis points, the lowest since September 2004, has diminished the relative attractiveness of Indian bonds compared to US treasuries.

The RBI’s Predicament: When Monetary Policy Hits Limits

The central bank finds itself in an unprecedented position. Despite deploying both traditional tools (rate cuts) and unconventional measures (massive bond purchases), the monetary transmission mechanism is clearly impaired.

This breakdown has serious implications:

- Credit markets remain tight despite policy easing

- Corporate borrowing costs stay elevated, undermining the growth recovery

- Policy credibility faces questions as tools lose effectiveness

The RBI’s challenge is compounded by the fact that it’s fighting structural issues—fiscal imbalances and external shocks—with cyclical tools designed for different problems.

Strategic Navigation for Different Stakeholders

Bond Investors: Duration Risk and Tactical Positioning

The current environment favors a defensive duration strategy. Short-term bonds (2-3 years) offer better risk-adjusted returns than long-duration securities. Corporate bonds with spreads of 150-200 basis points over government securities may provide attractive opportunities for investors willing to accept modest credit risk.

Equity Markets: Sectoral Rotation Imperative

Rising bond yields create clear winners and losers in equity markets:

Vulnerable sectors:

- Banks and NBFCs facing net interest margin pressure

- Auto companies dealing with higher financing costs

- Real estate struggling with mortgage rate increases

Defensive positioning:

- FMCG companies with stable cash flows

- Utilities with regulated returns

- Healthcare with non-cyclical demand patterns

Fixed Deposit Investors: The Silver Lining

For conservative savers, rising yields eventually translate to better fixed deposit rates. Those with short-term liquidity can wait for higher rates to lock in attractive returns once the cycle stabilizes.

The Precious Metals Opportunity: Gold and Silver in Focus

Rising bond yields and fiscal uncertainty create a compelling backdrop for precious metals, particularly in the Indian context where gold and silver have deep cultural and financial significance.

Currency Debasement Hedge: The combination of fiscal deficits, potential rupee weakness from trade disruptions, and massive government borrowing creates an environment where precious metals serve as natural hedges against currency devaluation.

Central Bank Buying: Globally, central banks have been significant buyers of gold, with countries like China, Russia, and Turkey accumulating reserves. This institutional demand provides a floor for prices even during temporary corrections.

Geopolitical Premium: The tariff tensions and broader US-India trade friction add a geopolitical risk premium to precious metals, as investors seek assets independent of any single nation’s monetary policy.

Looking Forward: Key Inflection Points

Immediate Catalysts (Sep-Dec 2025)

Oct and Dec MPC: With repo rate already at 5.50% (after a 100 bps cut already this year) and stance as “neutral”, I am not expecting any further repo rate cuts in the next two MPC meetings this year.

GST Council Decisions: The final implementation timeline for GST 2.0, originally targeted for Diwali 2025, will provide clarity on revenue impact.

Growth vs. Fiscal Trade-off: Q1 GDP data was announced on Friday and exceeded expectations massively, coming in at 7.8%. It will be interesting to see if another good news will bring bond yields down or not on Monday. Q2 GDP data will further reveal whether the fiscal stimulus is generating sufficient economic momentum to justify the revenue sacrifice.

Global Policy Shifts: Any change in US Federal Reserve policy could dramatically alter capital flows and yield differentials.

Medium-Term Scenarios (2026)

Optimistic Path: Government demonstrates fiscal discipline despite tax cuts, export markets diversify away from US dependence, and global trade tensions ease. In this scenario, RBI’s liquidity measures could eventually stabilize bond markets.

Risk Path: Fiscal deficit overshoots targets, tariff wars escalate, inflation resurges forcing monetary tightening, and foreign investor sentiment turns decisively negative on India.

The Verdict: What Bond Markets Are Really Saying

The current divergence between accommodative monetary policy and rising bond yields represents more than a technical market anomaly. It reflects a fundamental tension in India’s economic management between short-term growth support and long-term fiscal sustainability.

The bond market is essentially demanding answers to critical questions:

- How will the government fund tax cuts without compromising fiscal targets?

- Can India’s export economy withstand intensifying trade wars?

- Will inflation remain benign if fiscal spending increases?

There are other questions as well concerning overall geopolitical scenario, but it will have to be looked separately outside this article. Until these questions find convincing answers, bond yields are likely to remain elevated regardless of RBI’s monetary stance.

For investors, the lesson is profound: watch the bond market—it often reveals economic stress before other indicators. The current yield behavior suggests that India’s policy response must go beyond monetary accommodation to address fiscal and structural challenges.

The bond market doesn’t lie. Right now, it’s telling us that despite positive headlines about rating upgrades and tax cuts, the underlying economic equation faces serious stress. Smart investors will heed this warning and position accordingly.

In the complex world of financial markets, sometimes the most important signals come not from what’s rising, but from what should be falling but isn’t. Indian government bond yields are sending exactly that kind of signal today.

Disclaimer: I am not a registered SEBI Research Analyst and anything in the above article should not be construed as a recommendation. This should be read solely for education purposes.