Of Markets, Music, and Momentum

Here’s what’s inside this edition:

- Market Kya Lagta Hai: Nifty50 snapping 6-week losing streak, record low inflation, Trump Putin meeting

- Dil Se Paisa: Risk profile should be broken into risk taking ‘ability’ and ‘willingness’. Understand how it is important to set your asset allocation

- Inside Edge: ‘Hearing’ what Indian Music Industry sings to us

- Charts pe Charcha: TIPS Music, SML Isuzu and Eternal (Zomato)

- Brain ka Bazaar: The weekly quiz question__________________________________________________

Market Kya Lagta Hai

Nifty50 Finally Snaps Losing Streak

After six straight weeks of declines, the Nifty50 index rebounded this week, gaining 1.1% during a shortened, 4-day week marked by Friday’s closure for India’s 79th Independence Day. Broader indices Nifty Midcap and Smallcap also rallied, though gains were relatively modest compared to the headline index. This bounce gave traders a breather and signals cautious optimism, as large-cap stocks continued to lead the market’s recovery.

Sector Spotlight

Healthcare and Pharma outperformed, rising nearly 3% on strong earnings and renewed interest in defensive plays. Meanwhile, consumer durables lagged, declining by 2.1% as mixed results and muted festive prospects dampened sentiment.

Retail Inflation: Cooling Off vs Warming Up

India: India’s retail inflation fell to its slowest pace in 8 years in July, as CPI rose just by 1.55% YoY, slipping below the lower end of the RBI’s 2–4% target range for 5th straight month. While the moderation gives the RBI room to maintain a growth-supportive monetary stance, it also signals potential pressure on consumption due to lower farm incomes.

US: In contrast, US consumer prices rose 2.7% in July from a year earlier. While Fed officials had earlier worried that steep tariff hikes could push inflation higher, the absence of a sharper acceleration in price pressures likely removes a key obstacle to lowering rates amid concerns over a slowing labor market.

Market Implications: Lower inflation supports equities and debt markets, but subdued price growth may weigh on nominal GDP, corporate earnings, tax revenues, and credit expansion.

All Eyes on the Trump–Putin Meeting in Alaska

All eyes this week are fixed on Alaska, where U.S. President Donald Trump and Russia’s Vladimir Putin are holding a high-stakes summit focused on a possible ceasefire deal for the Ukraine war (by the time you might be reading this, the meeting would have been done).

The summit is taking place at Joint Base Elmendorf-Richardson in Anchorage, chosen for both its history and security. Early signs point to tough negotiations, with issues ranging from territorial concessions, sanctions relief, and energy supplies on the table. Observers, including Ukraine and European partners, are closely watching, not just for immediate headlines but for broader signals about global security and energy markets.

The meeting marks the first direct talks between the leaders since Trump’s return to office. While geopolitical hopes are high, any substantial breakthroughs or shifts in market sentiment will hinge on post-summit developments and the outcomes for global trade, oil prices, and regional alliances.

In case you would like to know interesting facts about various financial services topic, you should join the WhatsApp Channel. The latest post revolves around why Alaska was chosen as the meeting place and not, say, Washington DCBanking News: ICICI’s Minimum Balance Drama

56 years after India nationalized 14 private banks, arguing that private lenders of the time were too elitist to serve common citizens, ICICI Bank’s new minimum balance requirement of ₹50,000 on Savings Account re-ignited the same debate again.

The bold move was reversed days later seemingly due to widespread backlash. Consequently, the new minimum balance requirement is revised down to ₹15,000, still the highest among large banks.

Dil Se Paisa | Risk Taking Ability vs. Risk Taking Willingness

This is The Real First Step in Asset Allocation

When it comes to building a portfolio, risk profiling isn’t just a box-ticking exercise. The real insight comes from splitting risk into two parts:

- Risk Taking Ability: How much risk you can afford, based on hard financial facts.

- Risk Taking Willingness: How much risk you’re truly comfortable taking, shaped by emotion, temperament, and life experience.

These may sound similar, but they’re fundamentally different—and you need clarity on both to design an asset allocation that fits you, not someone else’s spreadsheet.

1. Risk Taking Ability — The Quantifiable Dimension

This is where the numbers come in: income, obligations, goals, liabilities, and timeline. It’s your real-world capacity to absorb losses without compromising your financial future.

Factors to assess:

- Current income and job stability

- Family dependents (kids, elderly parents, others)

- Big financial goals (home, education, retirement)

- Expected future income/business cash flows

- Liabilities: loans, EMIs, upcoming expenses

- Age and investment horizon

This is your head telling you logically, “You can afford this risk.”

2. Risk Taking Willingness — The Behavioural Side

Here, it’s all about your comfort with uncertainty and the prospect of loss. Upbringing, life shocks, temperament, and even daily mood influence how bold or cautious you feel.

Factors to recognize:

- Upbringing and formative influences

- Recent emotional events or shocks

- Risk temperament: anxious, adventurous, conservative

- Cultural background and family dynamics

- Current mood and mindset

This is your heart quietly asking, “Do you want to take this risk?”

Willingness is harder to measure and may fluctuate—sometimes changing overnight with major life events.

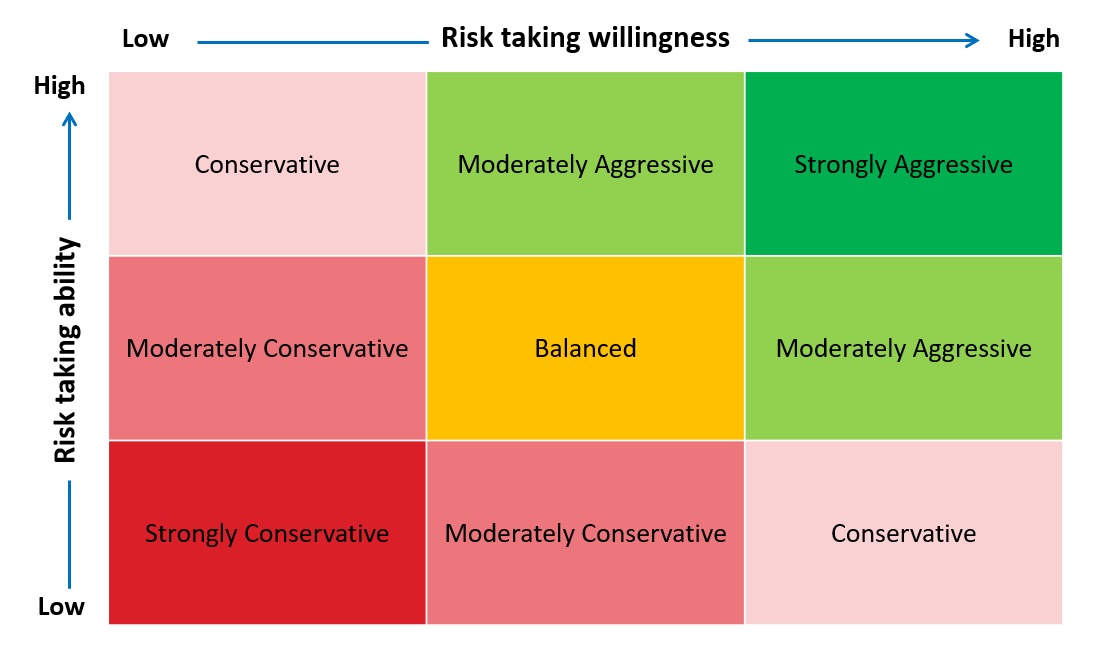

Why Balance Is Everything

If you build a portfolio only on ability, ignoring your emotional tolerance, you could find yourself panic-selling or sleepless when volatility hits. Conversely, a portfolio based just on willingness (without considering actual capacity) may leave you exposed to risks you simply can’t afford.

The sweet spot: Align the two, or at least understand where you fall short, so you can consciously compensate. You may refer to the following 3×3 matrix I created to understand what profile you might fall into.

Four Real-Life Risk Profiles:

Case 1 — High Ability, High Willingness

Sameer, 28, lives in Bangalore. With an IIT + IIM pedigree, he earns ₹3 lakh/month from his corporate job. He’s single, with zero liabilities, and came from a well-to-do family of entrepreneurs and journalists. No dependents, clean balance sheet, and both parents are financially independent.

- Ability: Very high—he has disposable income, no strings, and a decadal runway ahead.

- Willingness: Also very high—growing up without financial constraints, with choices, instills confidence. He enjoys calculated risks and views investing in growth assets as expected, not daring.

In short: Sameer has both the means and mindset to back aggressive allocations, including high-growth and concentrated equity positions.

Case 2 — High Ability, Low Willingness

Manjari, 25, just started as an investment banker in Mumbai after graduating from Wharton. She earns ₹4 lakh/month plus a year-end bonus. Her father had financed her education but tragically passed away recently, leaving behind partial education debt and a partially paid home loan. She has a younger brother in school and plans for marriage in 2–3 years.

- Ability: High—her compensation is strong and rising. Wharton credential gives her multiple career levers.

- Willingness: Low—she’s now the sole breadwinner. The emotional shock of losing her father, combined with growing responsibilities, has shrunk her risk appetite overnight.

In her case, despite a booming ability to take risk, her current phase demands safety and flexibility. The rational head says “invest heavily,” but the cautious heart says “preserve, protect, pause.”

Case 3 — Low Ability, Low Willingness

Sunil, 45, lives in Nagpur with his wife (homemaker), two school-going kids, and aging parents dependent on him for health care. He earns ₹65,000/month, services a car loan EMI, has no homeownership, and juggles high medical expenses for his father (with chronic ailments).

- Ability: Low—steady income but stretched by obligations and insufficient safety nets.

- Willingness: Low—growing up in a Marathi-medium school in Satara, watching his factory-worker father struggle without a pension instilled lifelong frugality and financial caution.

Sunil cannot afford risk (ability), and is not psychologically comfortable with it (willingness). Only very conservative strategies suit him—capital protection, income orientation, and minimal equity.

Case 4 — Low Ability, High Willingness

Angad, 33, based in Bhopal, works as a mutual fund distributor. His client base is small, his income barely pays the bills. He’s estranged from his well-to-do family and survives on his earnings. He hopes to marry soon but feels he needs financial momentum first.

- Ability: Low—less stable income, no family support, minimal reserves.

- Willingness: High—he’s a risk-taker by nature, grew up not valuing money, and is comfortable with high-stakes bets. He prefers gambling environments—stocks, derivatives, high-risk options.

Angad is willing to take huge swings, but practically, he may run into ruinous outcomes. His emotional willingness isn’t matched by financial capacity.

Takeaway for Investors

Before you debate which stock, asset class, or SIP amount is “right,” start with true self-awareness: know both your risk taking ability and willingness. This is your real starting point for designing a strategic asset allocation that can weather volatility—while keeping you genuinely comfortable along the journey.

Is your risk profile built more by your head or your heart? Getting this right is the foundation of smart, personalized investing.

Inside Edge

India’s Music Industry in 2025

India’s music industry is growing fast, valued at ₹53 billion in 2024 and expected to reach ₹78 billion by 2026. Film music dominates with about 80% of revenues, but non-film artists are gaining ground thanks to digital platforms.

Live music events surged 18% in 2024, with concerts like Coldplay’s Ahmedabad show generating ₹6.4 billion in economic impact. YouTube leads music consumption with 550 million users, mostly on ad-supported models, creating monetization challenges.

Companies like Saregama and Tips Music are innovating with large catalogs and digital products while delivering strong stock performance.

The big question remains: can India’s vast music audience be monetized fully?

The Rhythmic Revolution: India’s Music Industry Hits a High Note

·

14 August 2025

Music is woven deep into the fabric of Indian life. Its diversity spans language, region, and culture, yet its magic and emotional connection remain universal. The industry behind this heartbeat, however, is anything but simple. It’s a dynamic, tangled web of old-school record labels, film studios, streaming platforms, billion-plus listeners, live event…

Charts pe Charcha

1. TIPS Music

TIPS Music is tracing some textbook chart patterns! Its recent price action shows remarkable respect for Fibonacci retracement levels—38.2% and 61.8% have acted as support and resistance multiple times. There’s also a striking Head and Shoulders pattern, with the price hitting the theoretical target almost to perfection. To add to the technical intrigue, the stock is now consolidating within a narrow rectangle, forming a tight channel. Chart enthusiasts: can you spot H&S pattern?

2. SML Isuzu

SML Isuzu has delivered a stunning 325% return in under six months from its recent low. The fireworks didn’t stop there—after breaking out of a major long-term resistance, it doubled in price again within less than six weeks! An explosive uptrend and a great case study in momentum-driven rallies.

3. Zomato

Zomato is serving up a classic—the cup and handle pattern—with a convincing breakaway gap confirming the bullish setup. This formation is often watched closely for its potential to trigger sustained upside and signals strength in the underlying trend.

All observations are educational, not recommendations.

Brain ka Bazaar

Quiz Question:

POLL

Which of the following companies has never completely changed its business model?

Zomato (Eternal)

33%

Myntra

11%

In Mobi

22%

Tech Mahindra

33%

POLL CLOSED

Last week’s answer was Bombay Burmah Trading Corp and was correctly answered by 61% of respondents. Really amazing.

See you next week!

Disclaimer: I am not a registered SEBI Research Analyst and none of the constituent of this newslettter should be construed as a recommendation. This should be consumed solely for education purposes.