Fixing a Real Problem or Creating a New One?

The Indian mutual fund industry is no stranger to regulatory evolution. In fact, SEBI has, over the past few years, made significant moves to simplify mutual fund offerings and protect retail investors from overwhelming complexity.

One such milestone was the categorization and rationalization framework introduced in 2017, which allowed only one scheme per category per AMC, barring a few exceptions (like index, ETFs, FOFs, and sectoral/thematic funds). This greatly reduced clutter, eliminated duplicate schemes, and made investor choice easier.

Then, they came up with something in Nov 2020, which was around introduction of Flexicap funds (within equities) and changing the structure of Multicap funds.

However, now SEBI is considering a partial reversal to its 2017 framework.

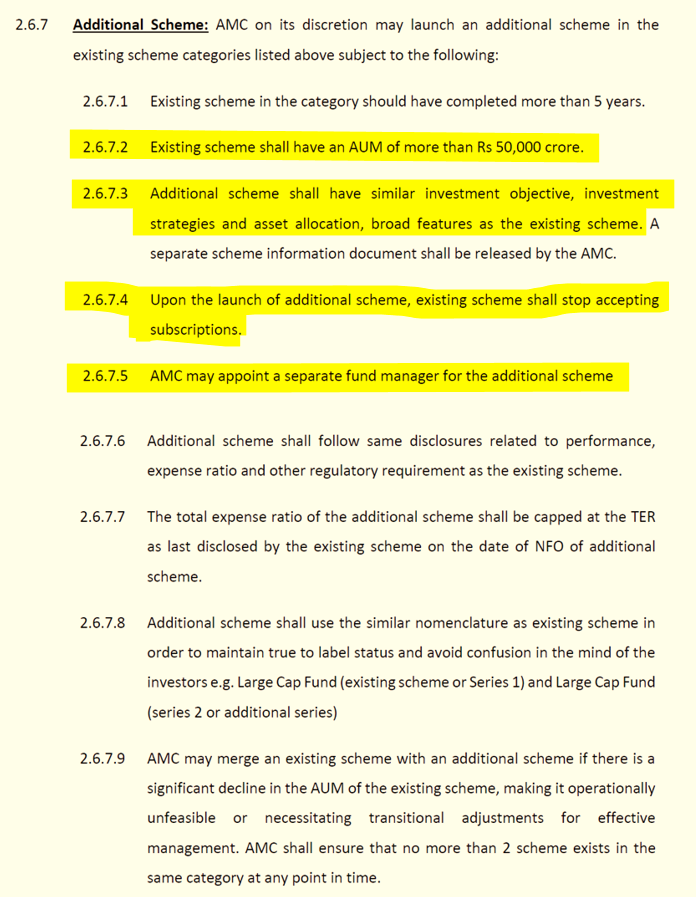

What Does Clause 2.6.7 Say?

In its 18th July 2025 draft circular on Mutual Fund Category Rationalization, SEBI proposes:

To allow AMCs to launch an additional scheme in a category if:

- Their existing scheme in that category has AUM ≥ ₹50,000 crore, and

- Has been in existence for at least 5 years

This move applies only to such high-threshold scenarios and would, in effect, make a handful of fund houses eligible today.

So far, only 9 active mutual funds (e.g., Parag Parikh Flexi Cap, HDFC Flexi Cap, HDFC Mid Cap, Nippon Small Cap, etc) have AUMs in this range.

What’s the Intent?

SEBI appears to be acknowledging the operational and investment constraints faced by extremely large funds.

Once a fund becomes huge (₹50,000 crore+), the ability to maneuver, take small-cap positions, or even outperform the index diminishes. With one-fund-per-category rule in place, fund houses may feel locked in, unable to launch an alternate strategy or cater to investors with different risk profiles. Few funds like SBI Small Cap or Mirae Large and Mid Cap have capped the SIP amount and disallowed lumpsum.

✅ The Case For a Second Scheme

Despite criticism, there are some practical reasons this could make sense:

1. AUM Bloat Becomes a Performance Drag

Managing ₹50,000+ crore within a single strategy can result in:

- Limited stock selection (can’t enter low-float or small-cap names with a meaningful position sizing)

- Too much cash allocation, even if it’s 1%, it becomes ₹500 crores

- Forced “indexification” of the portfolio, given they need to have so many stocks; Nippon Small Cap has 235 stocks

Splitting the corpus into two strategies may improve agility, reduce concentration, and allow more tailored positioning.

2. Two Fund Managers, Two Brains

One AMC might have two strong portfolio managers with different granular philosophies under same investment style

3. More Stock Ideas, Less Room

Fund managers often identify promising stocks but can’t include them due to position size limits, risk rules, or sector caps. A second scheme could offer a fresh canvas to deploy research insights without diluting the first fund’s core strategy.

4. Succession Planning / Talent Utilization

Allowing a new scheme lets AMCs give independent charge to promising fund managers. It fosters bench strength and prepares for succession, similar to how multiple CIOs handle verticals in PMS or AIF setups.

❌ The Case Against It (And Why the Critics May Be Right)

1. Cannibalization Risk

Launching a second scheme might result in:

- Redemptions from the first fund. There may be investors who would want to shift to the newer one

- Confusion among existing investors about which to choose

- Temporary underperformance as corpus shifts and volatility spikes

However, there can also be a possibility, that fund manager of existing scheme may shift to become fund manager of additional scheme, given no new fund inflows in existing will limit his potential. In that way, the existing will likely be managed by a newbie. Investors who invested in the scheme because of the star fund manager will look to shift (or exit because of confusion).

2. Undermines the Spirit of Categorization

The 2017 framework was designed to simplify choices. If multiple Flexi Cap or Large Cap funds return, we’re back to square one. AMCs offering dozens of similar-sounding funds with no clear distinction.

It raises a fair question:

Why even have a category framework if large AMCs can bypass it once they hit size?

3. Same House, Conflicting Calls

Imagine this:

- Fund A buys Reliance, as fund manager is bullish

- Fund B already had Reliance but is now selling, as fund manager is bearish

Both are managed by the same AMC. What message does that send to investors?

It erodes investor trust and raises governance questions on how consistent a fund house’s philosophy really is.

4. Second Fund May Likely Be “Inferior”

Let’s face it, the first fund is the flagship, with:

- Established track record

- Best allocation of investor trust

- First choice Fund manager with track record, managing it

A new fund may always feel like the “B team”. Why would rational investors shift?

5. Limited Need, Disproportionate Complexity

This rule may benefit only 9 equity funds in the entire industry today (additional 6 between ₹40-50,000 crore. But if it leads to equivalent new launches, we’re simply adding noise, especially at a time when SEBI is pushing for simplification in categories, TERs, and disclosures.

So, Is This a Good Move?

The answer isn’t binary.

Yes, massive funds do face real challenges and giving them flexibility might make sense.

The concern is that this clause could become a slippery slope, first 2 Flexi Cap funds, then 2 Large Caps, then 2 Mid Caps… and so on.

However, I would agree with SEBI’s thoughts of doing something sensible given the scenario so much funds are flowing into Mutual Funds now, and the star schemes will always invite most AUM.

Final Thoughts

SEBI has been a strong guardian of investor-first regulation. But this clause, though well-intentioned, may open the door to brand confusion, product duplication, and diluted accountability.

If anything, SEBI should think to launch and encourage fund houses to focus on new strategies like factor-based, or passives, for example. They should be encouraged to innovate within the structure, not replicate it.

What’s your view? Does this help the end investor, or only the AMC?